China’s GDP beats forecasts; Eurozone inflation accelerates; US production declines

China’s Q1 2026 GDP grew 5%, exceeding forecasts despite weak demand and geopolitical risks. Simultaneously, Eurozone inflation reached 2.6% due to high energy costs. Conversely, US industrial production fell 0.5% in March.

Chinese GDP growth exceeded expectations with a 5.0% year-on-year (YoY) increase in Q1 2026, bolstered by robust export performance which offset sluggish domestic consumption.

European Union inflation accelerated to 2.6% in March, fuelled by rising energy prices and supply-chain disruptions stemming from the ongoing geopolitical conflict in the Middle East.

US industrial production contracted by 0.5% in March, failing to meet analyst forecasts as the broader manufacturing and mining sectors faced a downturn.

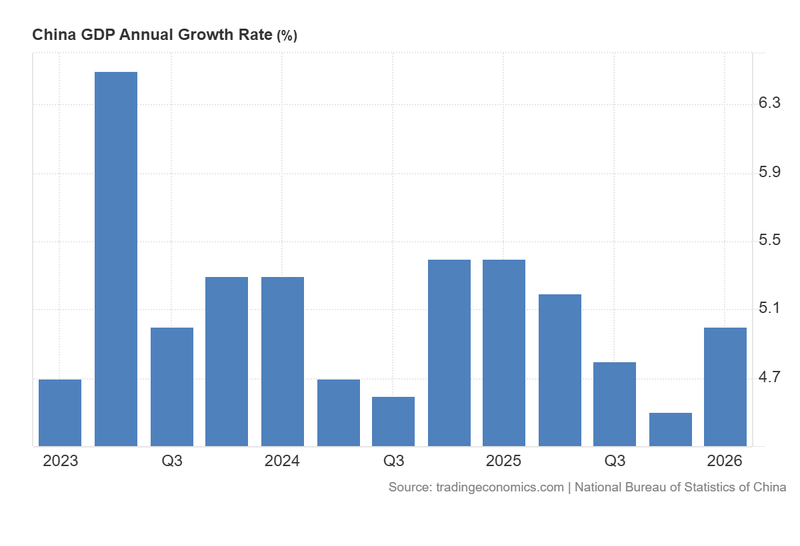

Chinese GDP surpasses analysts’ expectations and signals economic resilience

According to data released by the National Bureau of Statistics (NBS) of China, the year-on-year (YoY) Gross Domestic Product (GDP) growth rate rose by 5.0% in the first quarter of 2026. This figure outperformed the analyst consensus of 4.8% and represented a notable increase from the previous reading of 4.5%. This updated release reflects a quarterly expansion of 1.3%, marking the strongest quarterly advance since Q4 2024. Despite this robust growth, the NBS cautioned regarding a complex imbalance between high industrial supply and weak domestic demand, suggesting that the Chinese economy remains heavily reliant on the strength of its export markets to sustain current production levels.

Regarding the international landscape, the agency indicated that the prevailing energy crisis in the Middle East has not yet significantly hindered the domestic economy. This resilience is attributed to China’s strategic use of its substantial oil reserves and the successful diversification of its energy imports, which has reduced its immediate reliance on Iranian petroleum. However, the nation remains vulnerable to a more severe supply-chain shock should the US-Israel-Iran conflict prolongs. Consequently, the Chinese government and the central bank are proactively implementing expansionary policies to provide a buffer for the broader economy.

Market sentiment responded positively to these developments, with major equity benchmarks rising in tandem. The FTSE China A-50 index increased by 1.02% to reach 15,488 points, while the Hang Seng index appreciated by 1.41% to close at 26,345 points.

Figure 1. China GDP Annual Growth Rate (2023–2026). Source: Data from the National Bureau of Statistics of China; Figure obtained from Trading Economics.

Eurozone inflation adjusted upwards, exceeding analyst estimates

Data from Eurostat reveals that the inflation rate in the Eurozone accelerated from 1.9% in February to 2.6% in March in its final adjustment, surpassing the analyst expectation of a 2.5% reading. This represents the highest inflationary level recorded since July 2024 and was largely propelled by a surge in energy prices. The European Union remains a particularly vulnerable region due to its significant dependence on foreign energy exports—specifically oil imports from the Middle East. This vulnerability is underscored by the current US-Israel-Iran conflict, which has caused severe disruptions to energy commodity supply chains.

In terms of market reaction, the euro depreciated marginally against the US dollar by 0.17% to trade at $1.1779. It is probably that the currency's modest movement was due to the final economic release not presenting a significant surprise relative to the preliminary estimates.

US industrial production decreases in March, falling below consensus forecasts

According to data released by the Federal Reserve, industrial production in the United States decreased by 0.5% month-on-month in March, reaching its lowest level since September 2024. This reading fell short of the analyst consensus, which had anticipated a modest increase of 0.1%, and stands in sharp contrast to the 0.7% expansion recorded in February. Consequently, the year-on-year change in industrial production eased from 1.2% to 0.7%, marking its lowest rate of growth since June 2025.

An analysis reported by Trading Economics highlights that manufacturing output—which accounts for approximately 78% of total industrial production—declined by 0.1%. Concurrently, the mining industry saw a contraction of 1.2%, while the utilities index dropped by 2.3%.

Following the release of the industrial production data, major US stock benchmarks rose in unison, driven by burgeoning hopes of a diplomatic resolution to the conflict in the Middle East. The S&P 500 gained 0.26%, the Dow Jones Industrial Average increased by 0.24%, and the Nasdaq 100 advanced by 0.49%. Simultaneously, the US Dollar Index (DXY) appreciated by 0.13%. Thus, it appears that the reported declines in industrial output did not adversely impact market sentiment, as investors focused on broader geopolitical developments.