Central Banks brace for another inflation fight

How rapidly central banks are shifting back toward a more aggressive inflation stance after briefly hoping the energy shock might stay contained.

Christine Lagarde tried to strike a careful balance.

Andrew Bailey warned that waiting for second-round inflation before acting would be a mistake.

The 8-4 dissent was the largest division inside the Fed since 1990.

The ECB’s debate on Thursday made the picture much clearer

Several governors argued that more tightening will likely be needed unless the war ends quickly and oil prices reverse sharply. That matters because the discussion is no longer centered on whether inflation will rise. Policymakers already accept that. The debate is now about how deeply the energy shock risks spreading into wages, services and broader pricing behavior across the economy.

Christine Lagarde tried to strike a careful balance. She said the ECB still cannot clearly see second-round effects emerging yet, but she also emphasized that the central bank already knows where interest rates are headed. That is a subtle but important signal. It suggests policymakers may still be debating the speed of tightening, but not the direction.

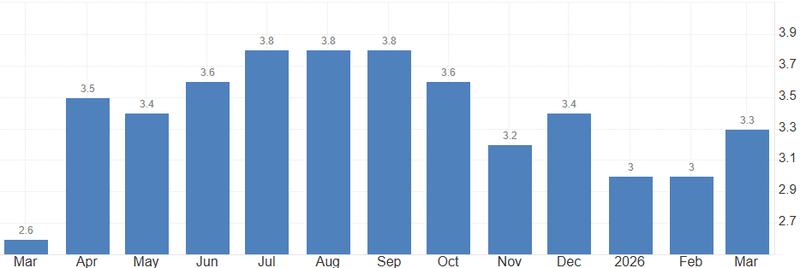

Source: EUROSTAT

The BoE sounded even more direct

Governor Andrew Bailey warned that waiting for visible second-round inflation effects before acting would be a mistake because, by then, it would already be too late. That is classic central-bank logic during supply shocks. Once inflation psychology becomes embedded in wages and pricing decisions, reversing it becomes far more costly.

Bailey’s remarks also revealed how policymakers are thinking about the oil shock itself. He said the more severe energy-price scenario now looks more plausible than the softer alternative. In other words, central banks are beginning to position around the idea that elevated energy costs may persist longer than initially hoped.

For much of the past year, markets believed central banks were nearing the end of tightening cycles as growth softened and inflation gradually cooled. The Iran conflict has complicated that narrative sharply. Policymakers are now confronting the possibility of weaker growth and renewed inflation pressure at the same time an uncomfortable mix that leaves rate-setters reluctant to sound dovish.

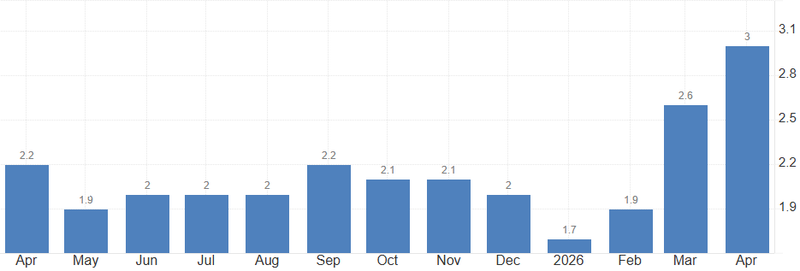

Source: Office for National Statistics

The latest Fed split shows how uncomfortable that environment becomes

The 8-4 dissent was the largest division inside the Fed since 1990. That is not a normal disagreement over fine-tuning policy. It reflects a genuinely fractured committee trying to judge whether inflation risks or growth risks now deserve greater weight.

Large dissents matter because they often signal that the consensus phase of policy is ending. During calmer periods, central banks usually move with broad agreement. Wide splits tend to emerge when the economic outlook becomes unusually uncertain or when policymakers believe the institution may already be behind the curve.

Energy shocks are particularly difficult for central banks because they hit both inflation expectations and real economic activity simultaneously. Tightening policy too aggressively risks damaging growth. Moving too slowly risks allowing inflation to spread far beyond energy itself.

That is why officials keep returning to the issue of second-round effects. The real danger is not oil alone. It is what happens if higher fuel, transport and input costs begin feeding into wages and core services inflation across the economy.

Once that process starts, central banks usually feel forced to respond much more aggressively later.

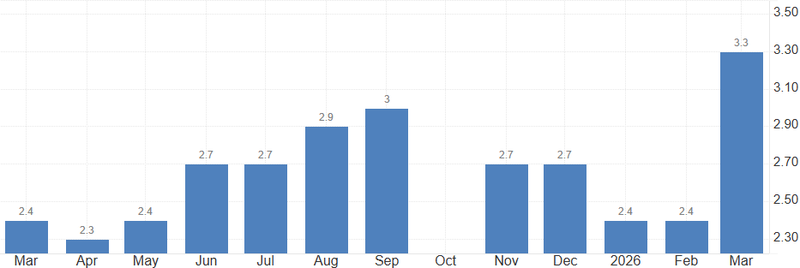

Source: U.S. Bureau of Labor Statistics

Markets are beginning to absorb that possibility again

A few months ago, investors were focused on when cuts would begin. Now the conversation has shifted back toward how many additional hikes may still be needed if the energy shock persists. That is a major repricing of the policy outlook in a very short period.

The deeper point is that central banks no longer sound like institutions preparing for normalization. They sound like institutions preparing for another inflation fight.