UK outlook Q1 2025

UK recovery: Dream or reality?

The UK economy faces a challenging 2025, with slow growth, persistent inflationary pressures, and global trade uncertainties clouding the outlook spilling in from 2024. The Bank of England (BoE) has forecasted a modest GDP expansion of 1.5%, underscoring the economic constraints from domestic challenges and Brexit's ongoing impacts.

Although there are some optimistic growth projections, the UK’s vulnerability to global trade shifts and inflationary pressures poses a risk of underperformance. Navigating this uncertainty will require close monitoring of domestic and international economic developments throughout 2025.

Global trade pressures and US policy changes

A significant challenge to UK growth prospects is the impact of shifting global trade patterns, particularly the policies of the incoming US administration.

While the UK is unlikely to be directly targeted by US tariff hikes, its open economy remains susceptible to broader protectionist measures and the ripple effects of increased tariffs worldwide. This vulnerability is compounded by the lingering effects of Brexit, which continue to disrupt trade and investment flows, further weakening economic performance.

Strengthening ties with either the US or the EU could provide some relief, but even closer cooperation may not fully compensate for the long-term challenges stemming from Brexit’s impact on trade relations.

The US remains a key trading partner, accounting for nearly 20% of the UK’s exports and imports. In 2024, the UK exported £188 billion in goods and services to the US while importing £116 billion. Despite this robust relationship, the UK’s negotiating position is relatively weak, leaving it highly dependent on US policies and exposed to potential external disruptions.

Monetary and fiscal constraints

On the domestic front, the UK government faces significant fiscal constraints. A high budget deficit, rising borrowing costs, and escalating public debt limit the flexibility to introduce fiscal stimulus measures. With limited room to manoeuvre, the government is restricted in its ability to support economic growth through public spending.

The Bank of England’s monetary policy options are similarly constrained. While there is potential for interest rate cuts, the BoE faces a delicate balancing act. Inflation remains sticky, and any additional rate cuts could spur inflationary pressures. Consequently, the UK's low productivity growth will further complicate a rapid recovery, meaning growth will likely remain subdued.

Inflation holds a steady grip

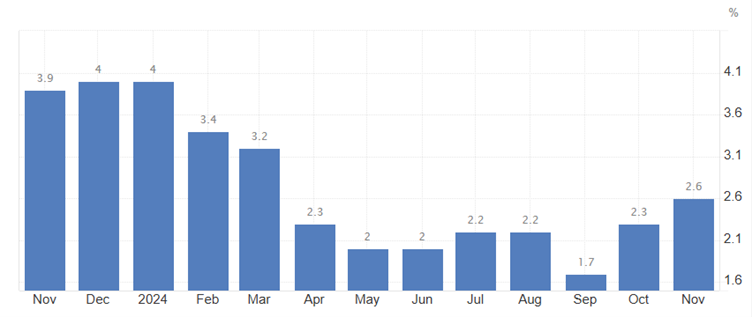

Inflation remains a key concern in the UK’s economic outlook for 2025. In November 2024, the annual inflation rate rose to 2.6%, driven by wage growth and higher service sector costs, despite a slight easing in the labour market.

Unemployment stands at 4.2%, with wage growth still elevated at 5.2%. However, surveys indicate that businesses, particularly smaller firms, are scaling back their hiring plans, suggesting a potential softening of the labour market.

While core inflation has moderated from last year's peaks, the disinflationary trend remains in place. The BoE projects CPI to reach 2.7% in 2025, with a slight easing to 2.5% by 2026. Nonetheless, if labour market conditions weaken further and economic growth remains sluggish, inflation could undershoot these forecasts, complicating the BoE’s policy decisions.

(UK inflation rate-Trading Economics)

Markets expect more rate cuts in 2025

The BoE’s cautious approach to monetary policy was evident in 2024, with only two interest rate cuts: from 5.25% to 5% in August and from 5% to 4.75% in November.

Despite recent cuts, persistent inflation limits the BoE’s ability to reduce rates further in the near future. However, as the labour market weakens and wage growth slows, the likelihood of additional rate cuts increases. Markets are currently pricing in 50 basis points of cuts for 2025, which could offer some short-term support for the pound.

In early 2025, the pound may face renewed pressure, particularly if inflationary pressures ease while economic growth remains subdued. Weakening labour market conditions, slowing wage growth, and reduced consumption could accelerate disinflation, prompting the BoE to act more aggressively than expected. This could exacerbate downward pressure on the pound, reflecting the fragility of the UK’s economic outlook.