US outlook Q1 2025

The Federal Reserve’s cautious expected rate cuts, rising inflation risks, and Trump’s trade policies shape a complex economic outlook for 2025.

Fed cuts rates to 4.25%-4.50%, stressing flexibility.

Inflation forecast for 2025 raised to 2.5%.

Trump’s tariffs may boost inflation.

Fed’s rate cuts depend on 2025 data.

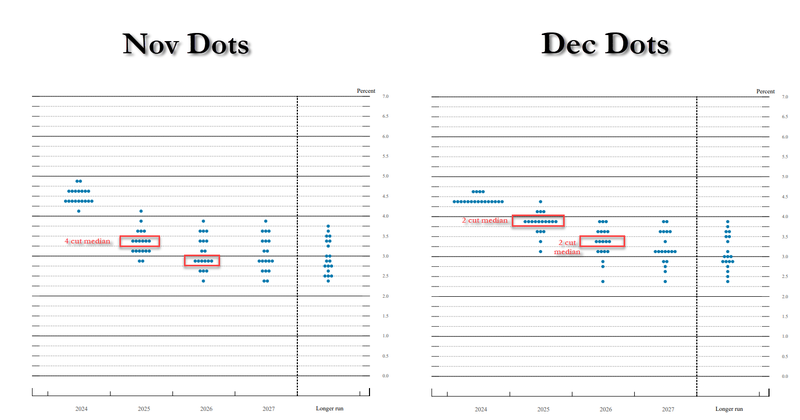

In December 2024, the Federal Reserve made a pivotal decision to cut interest rates by 25 basis points, lowering the target range to 4.25% to 4.50%. However, Chair Jerome Powell’s accompanying message was one of prudence, not celebration. While the Fed signalled two potential rate cuts in 2025, Powell made it clear that these would not follow a predetermined path, emphasising the importance of flexibility.

Source: FOMC

At the core of this approach lies the “neutral interest rate” that balances growth and inflation without excessively stimulating or restraining the economy. Powell acknowledged that current rates remain meaningfully restrictive, suggesting a slow and deliberate adjustment to monetary policy.

Inflation, debt and labour market

The Fed revised its 2025 inflation outlook, projecting core PCE inflation to hit 2.5%, up from the previous forecast of 2.2%. Key contributors to this uptick include the potential impact of President-elect Donald Trump’s trade policies and continued economic growth. These pressures reduce the urgency for sharp rate reductions but complicate the Fed’s fight against persistent inflation.

Fiscal challenges loom large with net interest payments on the federal debt reaching $870 billion in 2024, surpassing defence spending. The growing national debt of 36 trillion dollars raises questions about sustainability. As Treasury issuance is expected to increase in 2025 to cover growing deficits, upward pressure on long-term interest rates is likely to continue.

While the labour market remains strong, Powell highlighted a subtle loosening compared to pre-pandemic conditions. This shift could ease wage pressures, but it also signals vulnerabilities. Elevated interest rates continue to weigh on household and corporate finances, amplifying the risks to economic growth.

Awaiting Trump’s next move

President-elect Trump’s policy agenda introduces economic uncertainties, including a 20% tariff on imports from Canada and Mexico and a 10% tariff on Chinese goods, which could raise consumer prices and hinder the Fed’s inflation goals. These tariffs may disrupt major importers and exporters, slow GDP growth, and provoke retaliatory trade actions.

While proposed tax cuts may boost GDP and inflation, stricter immigration policies could raise labour costs, drive wage inflation, and limit economic growth. Together, these policies are likely to sustain upward inflationary pressure, challenging the Fed's ability to adjust interest rates while managing global debt demand and geopolitical risks.

Fed’s early 2025 agenda

The pace and extent of Fed rate cuts in 2025 will depend on economic data, unless unforeseen events like the COVID-19 pandemic occur.

Chairman Powell has emphasised that the Fed remains data dependent with a long-term inflation target of 2%. While major changes are unlikely early in the year, the March FOMC meeting could be crucial. A cut of 25 basis points could be considered if key metrics shift, reinforcing this data-driven approach. Powell noted that while inflation has made progress, it’s still moving sideways, and without a further slowdown in inflation, the Fed may proceed cautiously.

Meanwhile, ongoing inflation pressures from geopolitical fragmentation, expected Trump policies and heavy spending on AI and low-carbon initiatives are anticipated. Our outlook assumes a slight slowdown in the U.S. economy, while still in expansion, aligning with the Fed’s dual mandate. Combined with the country’s rising debt and deficits, this macroeconomic backdrop suggests long-term Treasury yields will likely remain higher for longer as investors demand higher compensation for risk.

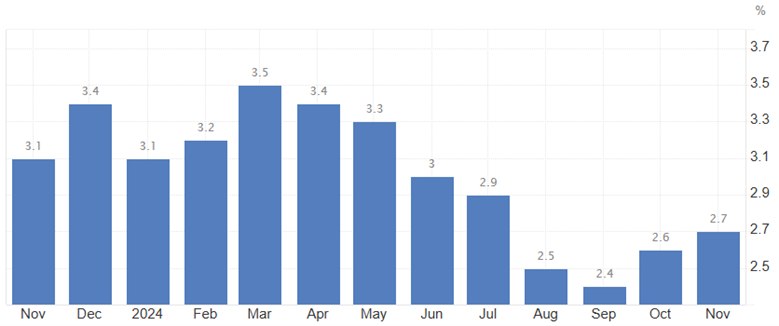

US inflation rate - U.S. Bureau of Labor Statistics

What’s next for the USD?

Despite expectations for modest rate cuts, the dollar is likely to remain strong relative to other currencies. If the Fed proceeds with fewer rate reductions than its global counterparts, the dollar will retain its appeal. Should the dollar index remain above 106.40, further gains toward 109.70–110.50 are plausible.