US treasury yields near 2007 highs as investors debate whether bonds are finally worth buying

Long-dated US Treasury yields are back near levels last seen before the global financial crisis, forcing investors into an uncomfortable choice. Some see a rare opportunity to lock in yields above 5%, while others argue the selloff is not finished and that inflation, deficits and policy uncertainty could still push long-end rates even higher.

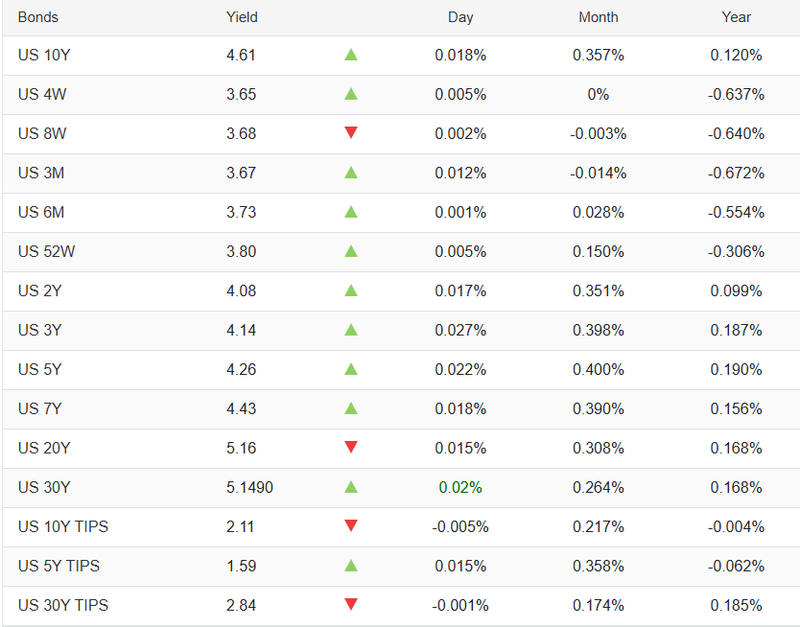

US 30-year Treasury yields are hovering near their highest levels since 2007.

Investors are split between buying attractive yields and avoiding further downside.

Higher energy prices, fiscal worries and sticky inflation are all weighing on long bonds.

Some strategists see value emerging, but many still prefer caution over conviction.

Long bonds are starting to look tempting, but few investors sound relaxed

The surge in long-dated Treasury yields is forcing bond investors into a tougher debate than they have faced in years. With the 30-year yield hovering around 5.13%, just shy of its highest level since 2007, the market is beginning to look attractive on paper. The problem is that it still does not feel safe.

Source: TradningEconomics

That tension is now defining the long end of the US rates market. On one side are investors tempted by the chance to lock in yields that would have looked unthinkable only a few years ago. On the other are those who believe the selloff still has room to run, especially if inflation stays sticky, energy prices remain elevated and fiscal concerns keep pushing term premium higher.

The bond market is trying to price two very different futures

The current move in yields reflects more than one story. Investors are trying to price the possibility that inflation proves much harder to kill, even with policy already restrictive, while also considering the risk that higher energy prices eventually drag growth lower. That combination has made Treasuries unusually hard to value with confidence.

The Iran war has added another layer of strain. Higher energy prices are feeding inflation concerns back into the market just as central banks are being forced to think again about how long they can stay patient. At the same time, the US economy has remained resilient enough to stop investors from rushing back into long-duration bonds as an obvious safe haven.

That is why yields keep grinding higher even when the market briefly flirts with de-escalation headlines.

Source: TradningEconomics

Value is beginning to appear, but conviction is still missing

There are now signs that some investors are starting to see value in Treasuries again, at least by certain metrics. But even those willing to acknowledge that yields have become more attractive are stopping well short of calling the all-clear.

The hesitation is easy to understand. A yield above 5% on a 30-year Treasury looks compelling only if it is close to the top. If the market is entering a new range and long-end yields are still adjusting upward, then buying too early can be expensive.

That is the core problem for investors now. High yields are drawing attention, but not yet trust.

The old demand zones are no longer holding

For much of this selloff, traders pointed to certain yield levels as likely magnets for demand. Around 4.5% in the 10-year and 5% in the 30-year were seen as areas where buyers might step in more decisively. But the market has pushed through both.

That matters because once those perceived support levels fail, investors have to consider the possibility that the long end is no longer anchored to the old framework. Instead, it may be moving into a new pricing regime shaped by larger deficits, more government borrowing, defense spending, sticky inflation and a central bank that looks increasingly boxed in.

If that is the case, then yield alone is not enough reason to buy duration.

The real concern is not just inflation, but confidence

One of the most important forces behind the selloff is the rise in term premium — the extra compensation investors demand to hold longer-dated debt. That rise suggests the market is becoming less comfortable with the broader policy backdrop, not just the inflation outlook.

Fiscal deterioration is part of that story. So is the sense that central banks are struggling to respond cleanly to repeated supply-driven shocks. Add in an energy crisis, political pressure on the Fed and an incoming chair expected to reshape how policy is communicated, and the market begins to ask for more compensation simply to stay long.

That is why some investors describe the global bond market as disordered rather than merely cheap. The issue is not whether yields are high. It is whether the forces driving them higher are close to fading. Right now, they are not.

Relief rallies still depend on the Middle East

The one clear path to a more durable bond rally would be a credible easing of the Middle East shock. That possibility has kept investors glued to every twist in the US-Iran story.

The market briefly showed how sensitive it remains to that outcome. Long bonds sold off sharply early in the week, then recovered part of the move on hopes that diplomacy could reopen the Strait of Hormuz and restore energy flows. Later headlines undermined that optimism. Then Donald Trump added another twist by saying he had called off planned attacks on Iran because “serious negotiations” were taking place.

Each of those headlines produced a reaction, but none delivered a lasting shift. Investors have now seen too many false starts to trust the first sign of progress.

This is why caution still dominates

The result is a market where value arguments exist, but feel fragile. Investors may like the absolute level of yields, but many are still reluctant to add duration outright without either a deeper selloff that truly breaks risk appetite or a credible reduction in geopolitical stress.

That is why some strategists prefer structures that cap downside rather than plain long positions in long bonds. The view is not that Treasuries cannot recover, but that the path back is still too uncertain to bet on with full conviction.

The market wants a reason to buy, not just a high number

For now, long-dated Treasuries are offering yields that look undeniably tempting. But this is one of those moments when a high yield is not a signal on its own. Investors want to know whether they are being paid generously for risk — or whether the market is warning them that something deeper is still unresolved.

That is what makes this moment so difficult. Bonds are starting to look cheap enough to matter, but not stable enough to trust.

And until energy pressures ease, inflation looks less threatening and the long end stops feeling untethered, many investors will keep looking at 5% plus yields and doing the same thing: admiring them from a distance.