US stocks fall as bond yields rise; China industrial output and retail sales slow

US stocks fell as rising Treasury yields and surging energy prices fueled global inflation fears and interest rate hike expectations. Concurrently, China's economic growth slowed sharply, with both retail sales and industrial production missing market forecasts due to geopolitical conflicts.

Rising US Treasury yields and escalating crude oil prices have reignited global inflationary fears, boosting the probability of further Federal Reserve rate hikes.

Major US indices retreated, led by technology and small-cap stocks, while the Dow Jones Industrial Average demonstrated resilience.

Chinese macroeconomic data missed consensus forecasts, with April retail sales growth decelerating to 0.2% year-on-year and industrial production slowing to 4.1%.

Investors are bracing for heightened volatility ahead of first-quarter corporate earnings from Nvidia and Walmart, alongside critical global inflation prints and the release of the FOMC minutes.

US equities slip on rising Treasury yields amid heightened inflation risks

Global equity markets have exhibited renewed anxiety regarding inflationary risks and the prospect of central banks returning to restrictive monetary policy pathways. The yield on the benchmark 10-year US Treasury note touched 4.6%, marking its highest level in approximately one year. Concurrently, the 2-year Treasury yield climbed to the 4.08% zone, reaching its highest level since February 2025.

Simultaneously, market participants remain concerned over appreciating energy costs. The Brent crude futures contract (BRNN6) advanced by 2.70% to reach $112.17 per barrel, while the West Texas Intermediate (WTI) futures contract (CLN6) increased by 3.29% to settle at $104.45 per barrel. These gains come as the conflict involving the US, Israel, and Iran approaches its third month, with a diplomatic resolution between the parties remaining elusive.

This macroeconomic environment reveals that market participants are increasingly pricing in potential interest rate hikes ahead of upcoming Federal Reserve policy decisions. This shift could constrain US domestic consumption and pressure other global central banks to tighten policy within a broader context of pervasive global inflation. According to the CME FedWatch Tool, implied market volatilities now reflect a 42% probability that the Fed will enact a rate hike at the 4.0% threshold by its March 2027 meeting, which represents a shift in perspective from previous assessments.

At the closing bell, the S&P 500 index dipped by 0.07% to 7,403 points, while the tech-heavy Nasdaq 100 index fell by 0.45% to close at 28,994. Concurrently, the Russell 2000 small-cap index depreciated by 0.65% to 2,775, reflecting expectations that higher borrowing costs could disproportionately impact small and medium-sized enterprises. Conversely, the Dow Jones Industrial Average exhibited notable resilience, appreciating by 0.32% to finish at 49,690 points.

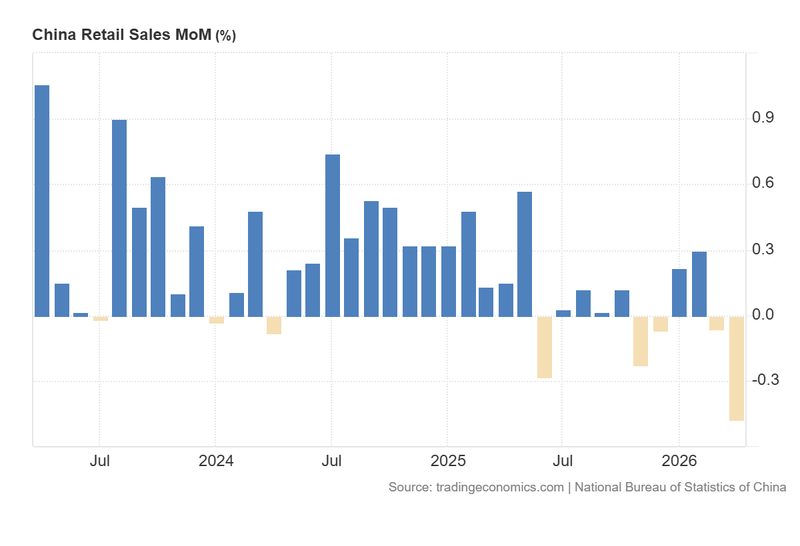

Chinese industrial production and retail sales decelerate below analyst expectations

Data released by the National Bureau of Statistics (NBS) of China revealed that retail sales contracted by 0.48% month-on-month in April, recording their weakest performance since October 2022. Consequently, year-on-year (YoY) retail sales growth decelerated from 1.7% in March to a mere 0.2% in April, substantially undershooting the market consensus which had anticipated an acceleration to 2.0%.

An analysis by Trading Economics indicates that this economic slowdown stems primarily from the ongoing conflict in the Middle East, which has severely depressed domestic consumer confidence. The contraction was most pronounced in big-ticket retail categories, including automobile sales, home appliances, building materials, and furniture. Conversely, categories such as tobacco and alcohol, communication equipment, and food products recorded gains.

Meanwhile, the NBS reported that industrial production growth decelerated from 5.7% to 4.1% YoY over the same period, missing the analyst forecast of a 5.9% expansion. The report highlighted that the mining and manufacturing sectors experienced the most significant easing, whereas the utilities sector—comprising electricity, gas, and water—accelerated in tandem. Chinese business confidence has similarly been weighed down by the geopolitical frictions in the Middle East.

Following the macroeconomic data releases, the FTSE China A50 index shed 0.71% to close at 15,533 points, while Hong Kong's Hang Seng index declined by 0.74% to finish at 25,612 points.

Figure 1. China Retail Sales (2023-2026). Source: Data from the National Bureau of Statistics of China; Figure obtained from Trading Economics.

Quarterly US financial results

The first-quarter 2026 earnings season continues this week. The following key institutions are scheduled to report, which may contribute to further volatility in the US equity markets:

Tuesday

- The Home Depot (HD)

Wednesday

- NVIDIA Corporation (NVDA)

- Target Corporation (TGT)

Thursday

- Walmart Inc. (WMT)

- Ross Stores (ROST)

Key economic events this week

Several critical economic indicators are scheduled for release this week, with the following being of particular importance to market participants:

Monday

- China: Industrial Production

- China: Retail Sales

- Japan: GDP Growth Rate

Tuesday

- United Kingdom: Unemployment Rate

- Canada: Inflation Rate

Wednesday

- United Kingdom: Inflation Rate

- European Union: Inflation Rate

- US: FOMC Minutes

- US: EIA Crude Oil Stocks Change

- Japan: Balance of Trade

Thursday

- US: Building Permits

- US: Housing Starts

- Japan: Inflation Rate

Friday

- Germany: GfK Consumer Confidence

- Germany: Ifo Business Climate

- United Kingdom: Retail Sales