US yields and dollar advance as inflation risks mount; Japanese PPI jumps sharply

Rising inflation risks and geopolitical tensions pushed US Treasury yields and the dollar higher, causing global stock markets to retreat. Higher energy prices and a potential hawkish Federal Reserve stance for 2026 dominate investor concerns, while Japan's PPI surged to a three-year high.

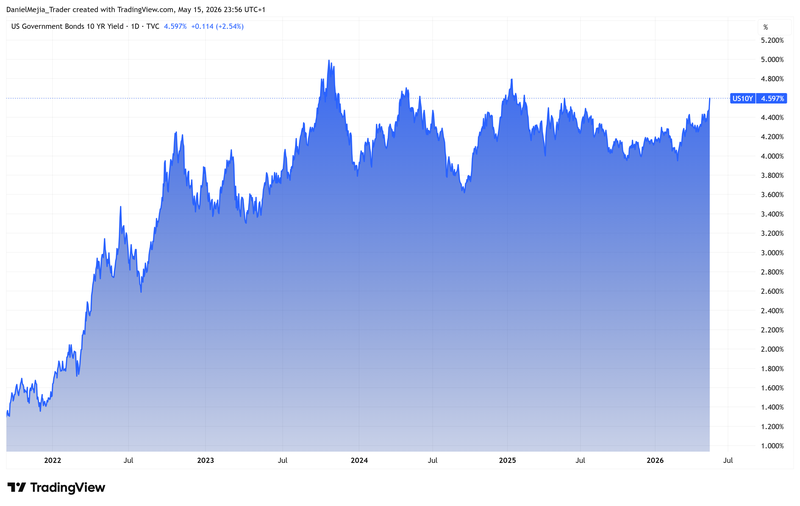

US 10-year Treasury yields hit a one-year high of 4.60% and the DXY rose to 99.27 points as investors braced for a more restrictive Federal Reserve.

Geopolitical tensions over the Strait of Hormuz pushed Brent crude up 3.35% to $109.26, raising doubts about a short-term US-Iran peace agreement.

Japan's corporate goods prices surged 4.9% year-on-year in April, hitting a three-year high due to energy pressures and a depreciating yen currency.

Resilient US industrial production grew 0.7% in April, but global stock markets fell sharply as investors prioritized mounting inflation risks.

US Treasury yields and dollar advance amid rising inflation concerns, while equity markets retreat

US Treasury yields and the US Dollar Index (DXY) advanced in tandem amidst escalating inflation risks and mounting expectations that the Federal Reserve could adopt an increasingly restrictive monetary stance. The 10-year US Treasury yield climbed 11.4 basis points to 4.60%, marking its highest level since May 2025, whilst the DXY appreciated by 0.40% to settle at 99.27 points.

Within the energy sector, global crude benchmarks rallied concurrently as doubts intensified regarding a near-term peace agreement between the United States and Iran. According to reports from Reuters, US President Donald Trump stated that his patience was "running out", adding that he had agreed with China that Iran must not be permitted to develop nuclear weapons and must reopen the Strait of Hormuz. Conversely, Iranian Foreign Minister Abbas Araqchi countered that Tehran remained open to negotiations only if Washington demonstrated serious intent, noting that Iran places no trust in the United States.

Consequently, the Brent crude futures contract (BRNN6) advanced by 3.35% to $109.26 per barrel, whereas the West Texas Intermediate (WTI) futures contract (CLN6) registered a marginal intraday decline but successfully defended the key psychological threshold to close at $101.02 per barrel.

According to the CME FedWatch Tool, market-implied probabilities have completely priced out any interest rate cuts for the remainder of 2026; notably, the probability of an additional interest rate hike at the December policy meeting has escalated to 41.3%.

Simultaneously, major US equity indices suffered synchronized losses at the closing bell. The S&P 500 shed 1.24% to finish at 7,408 points, the Nasdaq 100 index plummeted 1.57% to 29,125, and the Dow Jones Industrial Average fell by 1.07%. Meanwhile, European equity benchmarks retreated in unison under the weight of mounting inflationary anxieties: the French CAC 40 slid 1.60%, the UK's FTSE 100 declined by 1.71%, Spain's IBEX 35 depreciated by 1.05%, and Germany's DAX 40 dropped 2.07%.

Figure 1. US Government Bond Yields 10Y (2022-2026). Source: Own analysis conducted via TradingView.

Japanese PPI jumps to a three-year high amid energy price pressures

According to data released by the Bank of Japan, the Producer Price Index (PPI) jumped by 2.3% month-on-month in April, significantly overshooting market consensus estimates of a 0.7% expansion and marking its steepest monthly increase in over a decade. Consequently, the year-on-year (YoY) wholesale inflation rate accelerated sharply from a 2.9% in March to 4.9% in April, its highest level since May 2023. This rapid acceleration in corporate input costs exerts significant pressure on the Japanese central bank, which continues to face the dual challenge of rising structural inflation and fragile economic growth.

The PPI serves as a critical leading indicator for upcoming consumer inflation prints, as corporate price adjustments are typically passed down the supply chain to final consumers. For the Japanese economy, these intensifying inflationary pressures stem primarily from the dramatic surge in global commodity and energy prices, coupled with the persistent depreciation of the yen, which effectively imports inflation from major trading partners such as the United States.

In terms of currency market reactions, the Japanese yen weakened by 0.26% against the greenback to trade at ¥158.73 per dollar. This decline occurred amidst a broader rally in the US Dollar Index, driven by market participants expectations of a more restrictive Federal Reserve policy framework.

US industrial production accelerates beyond estimates, signalling economic resilience

According to data published by the Federal Reserve, US industrial production expanded by 0.7% month-on-month in April, comfortably beating analyst consensus forecasts of a 0.3% increase. Consequently, on a year-on-year basis, industrial output accelerated from 0.8% in March to 1.4% in April, underscoring the underlying resilience of the domestic economy. An analysis by Trading Economics notes that manufacturing output—which accounts for approximately 78% of total industrial production—grew by 0.6% on a monthly basis.

Although the robust industrial data indicates macroeconomic strength, market participants remain primarily focused on systemic inflation risks and upcoming monetary policy decisions from the Federal Reserve. This macro backdrop continues to generate widespread market uncertainty, exerting downward pressure on US equity indices into the closing bell.