Fed minutes reveal hawkish consensus; USD gains slightly

Most Fed officials maintained a restrictive stance, though two favored a cut. The dollar ticked up 0.13% as U.S. equities slipped 0.20% on average.

Fed minutes retain a hawkish tone during inflation-risk concerns; some members already eye cuts

WTI rose 1.6% after a larger-than-expected inventory draw tied to stronger demand

UK inflation beats forecasts again, increasing pressure on the BoE to reassess its rate-cutting plans

RBNZ cut its policy rate 25 bps on concerns about slowing growth

Fed minutes highlight a stronger hawkish tilt; dollar firms

The minutes showed an unusual split at the last meeting: Fed Vice Chair for Supervision Michelle Bowman and Governor Christopher Waller opposed holding the target range steady at 4.25%–4.50%, preferring a 25 bp cut amid weakening labor data—especially softer nonfarm payrolls in August and a three-year downtrend in hiring.

In contrast, the majority of committee members advocated for caution, referencing the likelihood of inflation rebounding as tariff impacts gradually reach consumers. FedWatch tool of CME Group now suggests a first interest rate reduction in September and a second in December, but the Fed's overall stance remains restrictive. Attention turns to Chair Jerome Powell’s remarks at Jackson Hole.

Crude inventories post a sharp draw; WTI climbs

Crude oil inventories tracked by the U.S. Energy Information Administration (EIA) posted a sharper-than-expected decline, highlighting stronger market demand. The agency reported a drawdown of 6 million barrels—well above analyst forecasts, which had anticipated a reduction between 1.3 and 1.8 million barrels. The larger-than-expected drop was attributed to increased refinery activity, stronger exports, and elevated demand from energy firms. Following the data release, WTI crude futures (CL) rose 1.6% after closing.

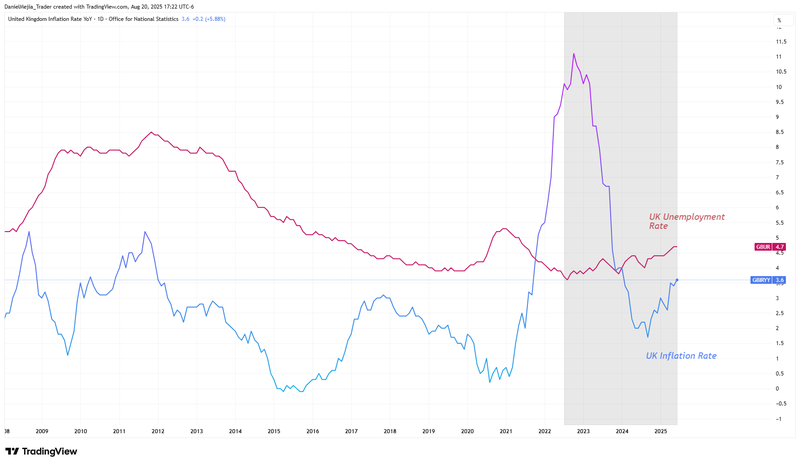

U.K. inflation picks up again, adding pressure on the BoE

Headline CPI accelerated to 3.8% YoY in July from 3.6%, above consensus. Core CPI (ex-food and energy) also rose to 3.8%. The British Pound eased roughly 0.25% as the upside inflation surprise complicates the BoE’s easing path, with the market weighing labor weakness more than rising prices (Chart compares rising unemployment since August 2022 with the inflation rebound since September 2024).

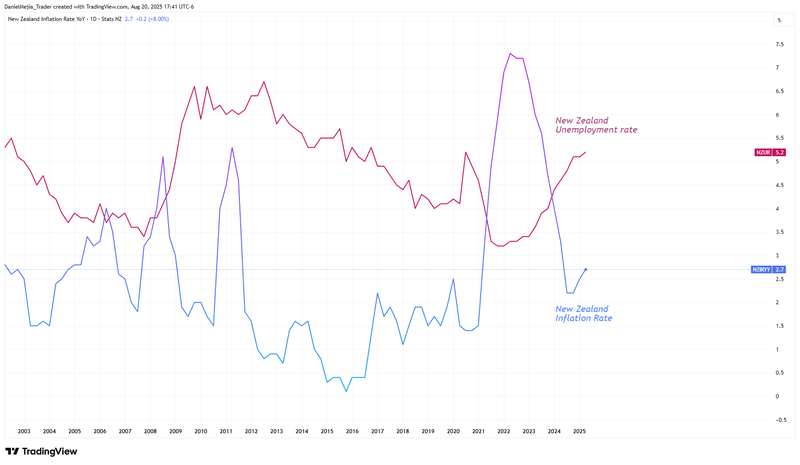

RBNZ cuts 25 bps on softer growth outlook

New Zealand’s central bank (RBNZ) lowered its policy rate by 25 bps to 3.00% and signaled further reductions in the coming months, citing a more challenging domestic and global growth backdrop. The RBNZ has now delivered seven cuts since its July 2024 peak of 5.50%. Inflation is nearing its target, but unemployment is rising more steeply in comparison to other advanced economies (Chart compares both indicators).