US inflation edges higher

Inflation concerns persist globally, as U.S. inflation ticks up and central bankers in Europe caution on growth and policy impacts.

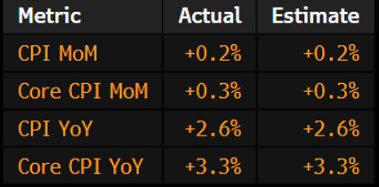

U.S. annual inflation rose to 2.6% in October, aligned with forecasts, led by rising shelter costs

Villeroy suggests ECB may consider further rate cuts amid inflationary pressures and rising French unemployment

The U.S. annual inflation rate increased to 2.6% in October, up from September’s 2.4%, staying within market expectations as steady rises in housing costs continued to drive the monthly 0.2% increase in consumer prices. Core inflation also remained consistent, holding at 3.3% year-over-year and 0.3% on a monthly basis. This aligns with stable inflationary momentum in core categories but highlights ongoing pressures in housing, which rose 0.4% and accounted for over half of the monthly rise.

In Europe, French ECB Governing Council member Francois Villeroy de Galhau expressed concerns today over the potential inflationary effects of U.S. policy changes under President-elect Donald Trump. Speaking with France Inter, Villeroy underscored the possibility that Trump’s economic agenda—particularly his inclination toward tariffs—could stoke inflation in the U.S. and present a broader risk to global growth. He suggested the ECB may explore rate cuts if inflation and growth continue to diverge from the bank's targets. Additionally, Villeroy noted a potential temporary spike in France’s unemployment rate to around 8%, before returning to more stable levels near 7%.

Villeroy highlighted Trump’s proposed tariffs, intended to address the U.S. trade deficit by levying a minimum 10% tax on all imports, as a policy that could dampen consumer purchasing power, potentially squeezing household budgets. “Protectionism almost always means reduced purchasing power for consumers,” he cautioned, noting potential global ripple effects that could affect Europe and China as well.

Meanwhile, Bank of England Monetary Policy Committee (MPC) member Catherine Mann reiterated her assertive stance on inflation control in a panel discussion, where she underscored the importance of a “go big” approach to monetary policy adjustments. Mann emphasized that recent studies point to quicker-than-expected impacts of rate changes on firms' pricing and inflation expectations, a view that could support more dynamic policy moves.

Holding firm on her cautious view, Mann pointed out the persistence of high inflation in services, indicating the risk of price volatility and underscoring her reluctance to ease policies until inflation pressures more clearly subside. “For those two reasons I say that inflation has not yet been vanquished,” she concluded.

Both Villeroy and Mann’s comments underscore a careful balancing act by central banks as they navigate complex inflation landscapes and policy challenges, driven by both domestic and international influences.