Fed between credibility, inflation, and the battle between policy and politics

Even the more dovish policymakers within the Federal Reserve are now warning that inflation remains uncomfortably high, underscoring a clear lack of urgency to act.

Warsh has also proposed changing the Fed’s inflation measurement framework.

If inflation rises above 5%, the Fed may be forced to adopt a more aggressive stance rather than wait and see.

The Fed is unlikely to rush into rate cuts as long as inflation remains a real threat.

Fed credibility

The Fed's most dovish policymakers now warn that inflation remains uncomfortably high, underscoring a lack of urgency to move, and what added the uncertainty is Kevin Warsh senate testimony that he refused to call the 2020 elections a loss for president trump that made people look at Warsh as human sock puppet but he asserted his independence from the white house denying that he made any deal to lower interest rate to pleasant trump.

He also proposed a regime change in how the fed measures inflation, that idea came because Warsh believes that AI is triggering a 1990 style productivity surge and allowing the economy to grow faster without triggering inflation a scenario that would permit lower borrowing costs, the trimmed inflation measure is a strategic way to align the Federal Reserve's math with Trump's demand for lower interest rates without appearing to sacrifice the Fed's 2% inflation mandate. On the other hand, it will provide a technical, data-driven excuse to cut rates, on the same time he uses the AI-driven productivity that allows the economy to grow faster without causing inflation so he can align with Trump's "growth at all costs" platform.

Inflation debate and political pressure

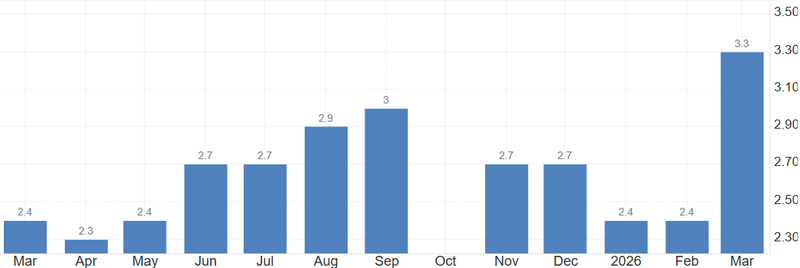

The latest expectations were signaled one rate cut in 2026, but with oil prices above $80.00 the uncertainty due to inflation having a second-round effect and printing a spike on the inflation made the fed tone signal to stay higher for longer tone until the end of 2026.

But with Warsh coming to the fed and trying to change how the inflation calculated Warsh can effectively ignore the inflationary impact of Trump's tariffs or energy price spikes, framing them as temporary "one-off" factors that shouldn't stop rate cuts it will not help much because if oil prices stays higher than average it will start leaking into other goods, the trimmed mean could eventually rise higher than the old formula, potentially forcing Warsh to raise rates later.

If inflation spikes above 5%, will force the fed to implement aggressive tone rather than using the wait-and-see tone even if that inflation number spike with Warsh as fed chair will let the statistical adjustments that Warsh wants, will look like political manipulation rather than sound policy. To protect his own credibility and prevent a 1970s-style spiral, Warsh would likely be forced to abandon his "productivity boom" theory and instead raise rates to "insure" that high inflation doesn't become a permanent fixture of the economy. This would create a significant clash with the White House, as the Fed would be forced to choose between supporting the President's growth agenda and stopping a runaway cost-of-living crisis.

Source: U.S. Bureau of Labor Statistics

Powell’s tone could anchor or extend market uncertainty

The tone in 29/April will make the market uncertainty to cool down and to know the path the fed is taking, Powell will hold the wait-and-see tone that is both patient and cautious, reaffirming the "higher for longer" narrative and will likely emphasize that the Fed is "squarely focused" on its dual rather than political timelines, Powell will likely distance himself from Kevin Warsh’s "trimmed" inflation theories, sticking instead to traditional Core PCE data to show that price stability has not yet been achieved.

Ultimately, his tone will be designed to assert central bank independence signaling to both the markets and the White House that the Fed will not be rushed into a rate cut while inflation remains a credible threat to the economy, however if Powell tried not to give any heads up about Q3 expectations and explicitly state that he "cannot make a prediction" about future policy and that rate hikes will not be the "base case’’ and leave it for Warsh to do that will make the market uncertainty phase to continue.