Markets are pricing peace, but the inflation risk is still around

U.S. President Donald Trump signaled that a deal could come soon, with talks potentially resuming over the weekend and even suggesting that the current ceasefire may not need extension if progress continues.

OPEC+’s production has fallen by around 7.7 million barrels per day.

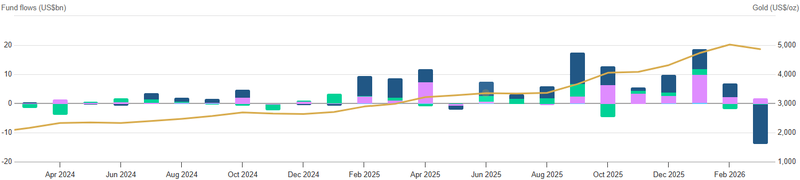

Gold ETF flows saw a net outflow of around $11.9 billion last month.

Inflation is unlikely to fall as quickly as markets expected.

Oil Is signaling a slower pricing

U.S. indices are trading back near previous highs, reflecting a market that is increasingly pricing in de-escalation. But the speed of that move is raising a more cautious question beneath the surface: has the market moved too early?

Because while headlines are improving, the underlying conditions that drove the initial shock have not fully reversed.

If markets were fully convinced that the conflict is ending cleanly, oil would be telling that story more clearly. Instead, crude remains elevated, still holding close to the $90 range. It suggests that even if the probability of full-scale disruption has declined, the physical market is still tight.

The disruption around the Strait of Hormuz has left a real dent in supply chains. OPEC+’s output dropped sharply, with production falling by around 7.7 million barrels per day in March at the peak of the disruption. At the same time, OPEC cut its Q2 demand forecast by 500,000 barrels per day, not because demand collapsed, but because the conflict itself distorted flows and consumption patterns.

This creates a situation where supply is constrained, but demand is also becoming less predictable. Even if tensions ease, shipping routes, insurance costs, and refinery adjustments all take time to normalize.

Peace priced in, but gold waits the fed’s signal

Gold is also starting to reflect this shift toward de-escalation, but in a more cautious way. Prices have not surged as they typically would during geopolitical stress, suggesting the market is already pricing a partial easing of tensions and a lower probability of escalation. However, gold’s direction right now is being shaped less by geopolitics and more by policy expectations.

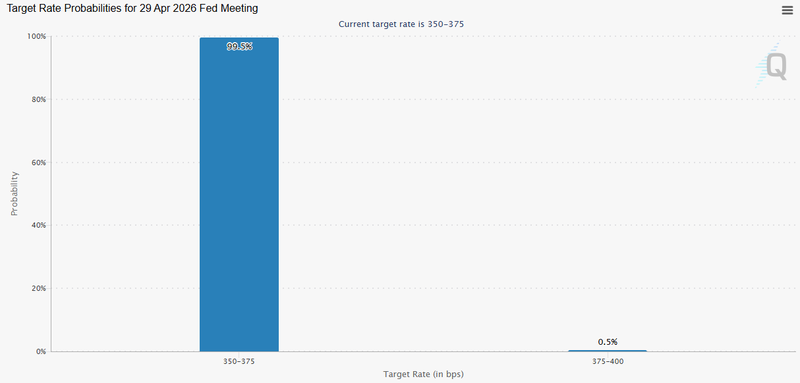

The focus has clearly shifted toward the April 29 Federal Reserve decision the base case is for no change in rates, but the tone of Jerome Powell will be the real signal for markets heading into Q2. Whether he leans toward patience or signals concern about persistent inflation will determine the next move not just for yields and the dollar, but for gold as well. That shift in focus is already visible in positioning. Gold ETF flows saw a net outflow of around $11.9 billion last month, indicating that investors have been reducing exposure as the immediate fear premium fades and attention turns back to interest rates and macro direction.

Source: Gold.org

Inflation risk does not disappear with a ceasefire

Energy feeds into inflation with a lag. Higher crude prices gradually pass through fuel costs into transportation, food, and manufacturing. That means even if geopolitical tensions ease, the inflation impact can continue building in the near term. If oil stabilizes near current levels, inflation is unlikely to fall as quickly as markets previously expected. There is a real risk that inflation remains sticky, or even higher, as delayed effects begin to show in upcoming data. More importantly, inflation and oil are not reacting to headlines alone.

Talks about ending the war may shift sentiment, but the physical market will wait for confirmation. The real signal is whether supply flows, especially through the Strait of Hormuz, return to normal and stay stable. Until shipping routes, insurance costs, and actual deliveries normalize, oil prices are likely to remain elevated regardless of diplomatic progress. This brings the April 29 Federal Reserve meeting into focus. The base case is for no change in rates, but the tone of Jerome Powell will be the key signal. Markets are no longer just looking for a decision; they are looking for direction.

Whether the Fed leans toward patience or signals concern about persistent inflation will shape expectations for the rest of Q2. Discussions from the March meeting already highlighted how the war could pressure both sides of the Fed’s mandate, pushing inflation higher through energy while also risking slower growth if costs weigh on demand. Markets were confident that rate cuts were coming. That view is now being questioned. If energy-driven inflation proves persistent, and oil remains supported by slow normalization of supply routes, the Fed has less room to ease, keeping policy expectations cautious.

Source: CME Group