Japan is caught between inflation pressure and growth risk

Japan is entering a more complicated phase, where external shocks are starting to matter more than domestic policy alone.

Middle Eastern supply routes raise Japan’s import bill almost immediately.

10-year yield rising to 2.415% points to longer-term inflation uncertainty.

April 28 may be more about signaling the next move than actually delivering it.

Japan’s energy shock is now a supply chain problem

The latest developments around energy prices and geopolitical tensions are forcing policymakers to navigate a narrow path between rising inflation and fragile growth. What makes this moment different is that Japan is no longer operating in a low-inflation vacuum. It is now exposed to the same global forces that are pushing prices higher elsewhere, but without the same economic flexibility.

The government’s move, led by Sanae Takaichi, to provide $10 billion in financial support to Southeast Asia is not just diplomacy, it is supply-chain defense. Japan remains deeply dependent on the region for critical imports, including medical supplies and industrial inputs. If energy-driven disruptions hit Southeast Asia, Japan feels it indirectly through shortages and higher costs. This is a proactive attempt to stabilize upstream partners before the shock feeds back into the domestic economy.

At the same time, the energy backdrop is becoming harder to ignore. Oil prices remain elevated, and any disruption in Middle Eastern supply routes raises Japan’s import bill almost immediately. Unlike the U.S., Japan cannot offset this with domestic production. That makes inflation more externally driven and harder to control through traditional monetary policy.

The BOJ faces a two-sided risk that is hard to price

Bank of Japan Governor Kazuo Ueda’s latest remarks reflect a central bank that is increasingly uncertain, not inactive. The market had been leaning toward a gradual normalization path but rising geopolitical risks have complicated that narrative. Ueda’s tone was cautious, explicitly highlighting both upside and downside risks, which is central to understanding the current policy dilemma.

On one side, higher oil prices create upside inflation risk. Energy feeds directly into Japan’s import-heavy economy, pushing up costs for businesses and households. This would normally justify tighter policy or at least continued normalization. But on the other side, there is a real risk that higher energy costs begin to slow demand. If households pull back and corporate margins compress, inflation could weaken again after an initial spike.

That is the core issue: inflation in Japan is still not entirely self-sustaining. It depends heavily on external cost pressures rather than strong domestic demand. This creates a scenario where tightening too early could choke growth, while waiting too long risks, allowing inflation expectations to drift higher.

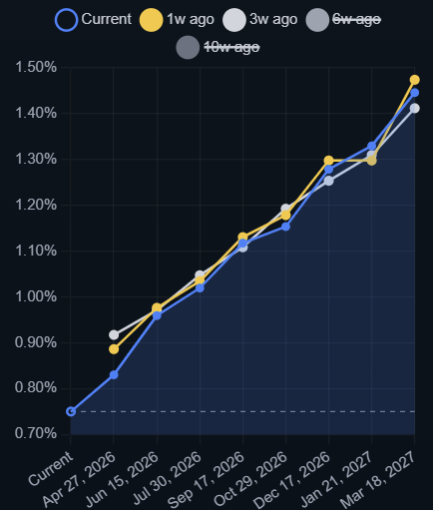

Bond markets are already reflecting this tension. The 2-year JGB yield, which is most sensitive to policy expectations, has edged slightly lower to around 1.365%, suggesting markets are dialing back immediate hike expectations. Meanwhile, the 10-year yield rising to 2.415% points to longer-term inflation uncertainty. This divergence shows that investors are not pricing a clear policy path, but rather a range of possible outcomes.

The next move depends on energy, not just policy

The Bank of Japan’s April 28 decision is now finely balanced between a rate hike and a hold, and the market is leaning slightly toward patience rather than action. Yields have been trending higher consistently, moving from around 0.75% previously toward the 1.4–1.5% range in forward expectations, but the move is gradual, not aggressive. That tells you the market believes normalization is coming, just not necessarily at this meeting.

A rate hike on April 28 is still on the table, but the bar is relatively high. For the BOJ to move now, it would need confidence that inflation is becoming more durable and less dependent on external shocks. The problem is that much of the current inflation pressure is still being driven by energy. Oil prices remain elevated, and for Japan an import-heavy economy that feeds directly into costs. But this type of inflation is unstable. It can rise quickly, but it can also fade just as fast if energy prices pull back. That makes it difficult for the BOJ to justify tightening purely on that basis.

If the BOJ does hike, it would likely be framed as a precautionary step, aimed at maintaining credibility rather than reacting to strong domestic demand. It would signal that policymakers are becoming less comfortable with staying behind the curve if inflation expectations begin to drift higher.

The more likely outcome, however, is no change with a hawkish tone. That would align with Governor Ueda’s emphasis on two-sided risks. On one hand, higher oil prices push up inflation. On the other, they risk slowing growth, especially through trade channels linked to Southeast Asia.

BOJ is likely to wait for clearer data. The path forward remains upward for rates, but April 28 may be more about signaling the next move than actually delivering it.