Iran talks leave markets stuck between diplomacy and war risk

Markets are no longer trading the Iran story as a simple geopolitical shock. They are now trying to price two paths at once: a negotiated deal that lowers energy risk, or a renewed military campaign that keeps inflation pressure alive and pushes long-dated bond yields even higher.

Vance said the US wants a diplomatic solution and believes progress has been made with Iran.

The U.S. Senate voted 50-47 to advance a War Powers Resolution to force Trump.

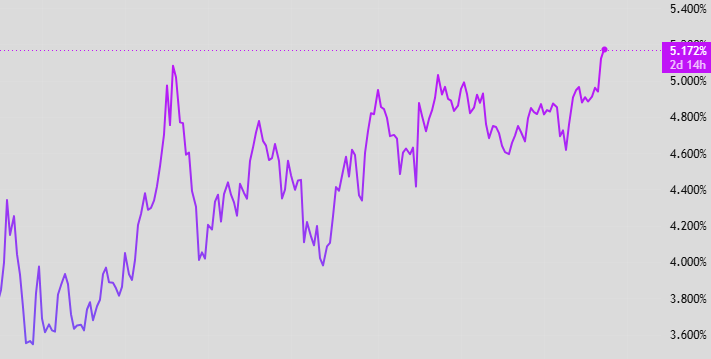

U.S. 30-year Treasury yield reached around 5.18%, its highest level since July 2007.

Washington is trying to keep both options open

The message from Washington is deliberately split. Vance said the US wants a diplomatic solution and believes progress has been made with Iran, but he also made clear that the military option has not disappeared. That is the part markets cannot ignore.

US is trying to negotiate from a position of pressure. The administration wants Iran to accept limits that prevent a return to nuclear weapons capacity, while keeping the threat of renewed strikes in the background. That may help force talks forward, but it also keeps risk premium alive across oil, bonds and equities. The market is not only asking whether a deal is possible. It is asking whether diplomacy can move fast enough before another military escalation resets the whole picture.

Congress is becoming part of the market story

The U.S. Senate voted 50-47 to advance a War Powers Resolution to force President Trump to halt military action in Iran, the Senate vote matters because it shows the Iran conflict is no longer only a White House decision in political terms. The resolution would force Trump to halt military action against Iran unless he receives explicit congressional authorization, although it still faces major hurdles, including the possibility of a presidential veto.

Voting is important even if it does not end the conflict. It signals that patience in Washington is thinning, and that any renewed military campaign may face a harder domestic political path.

Bond markets are not waiting for clarity

The clearest market reaction is still in long-dated government bonds. Long yields have been rising because investors are demanding more compensation for inflation, fiscal pressure and geopolitical uncertainty. In the US, the 30-year Treasury yield reached around 5.18%, its highest level since July 2007.

This is not just about one inflation print. War risks feed into energy prices, energy prices feed into inflation expectations, and inflation expectations make it harder for central banks to sound relaxed. At the same time, governments are borrowing more, which means investors are being asked to absorb more long-term debt at exactly the moment confidence is weaker. Yields are not rising only because growth is strong. They are rising because investors want more protection against a world that feels less predictable.

Source: Trading View

The war risk is keeping the long end untethered

Long-dated bonds usually benefit when geopolitical risk rises. But this time the shock is different. If the conflict threatens oil flow, raises energy costs and keeps inflation rising, then bonds do not behave like a clean haven.

That is why yields can keep climbing even while investors are nervous. The market is simply not running away from risk. It is questioning whether long bonds still offer enough compensation for the inflation and fiscal risk attached to them.

Japan is seeing pressure as well, with 10-year JGB yields recently jumping to record highs, while UK long-term gilt yields have also moved to levels not seen in decades.

This makes the Iran story global. It is not just about oil or the Middle East. It is about whether governments can finance themselves smoothly in a world where inflation shocks keep returning.

Source: Trading View