SpaceX IPO a great opportunity or bull trap?

SpaceX could become one of the most important companies in the world and still disappoint public investors. That is the uncomfortable part of the IPO story.

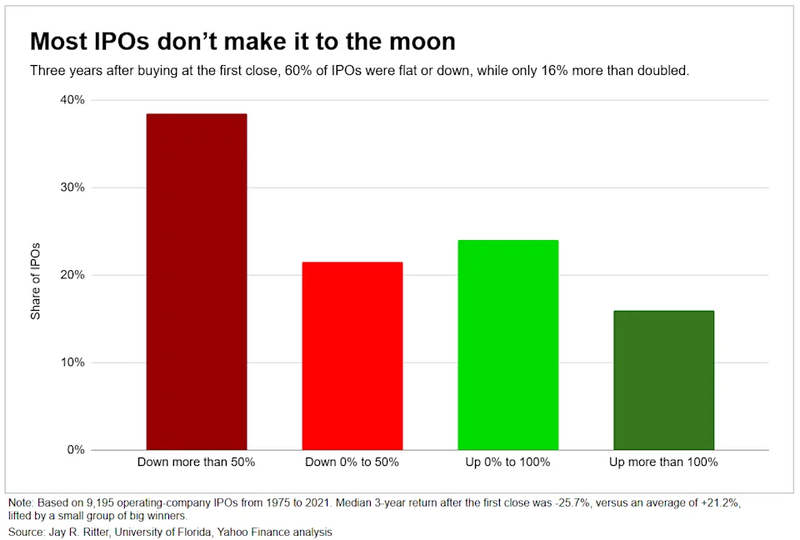

Historical IPO data shows many new listings struggle after the first trading day.

Investor demand is reportedly approaching four times the size of the planned offering.

SpaceX is targeting a valuation of about $1.75 trillion.

Is SpaceX’s IPO price already too high?

SpaceX is not coming to market as an early-stage growth story. This is not a small company asking public investors to fund its first major expansion. SpaceX has already changed the launch industry, built Starlink into a major satellite internet business and pushed into the AI infrastructure story. Much of that value has already been created in private markets.

At $1.75 trillion, SpaceX would already be priced as one of the largest and most important companies in the world. That does not mean the valuation is impossible to justify. But it does mean the stock would have very little room for disappointment.

A company can be exceptional and still become a difficult investment if too much of the future is already in the price.

Are public investors arriving too late to SpaceX?

The IPO will attract demand because SpaceX has been closed to most investors for years.

That scarcity matters. When a company this famous finally comes to market, investors do not only buy the financials. They buy access, the brand, the Musk premium and the fear of missing the next Tesla-style move.

Is SpaceX too mature to deliver Tesla-style returns?

Public investors would not be buying a small company before the market understands the story. They would be buying a mature private-market winner after years of value creation, at a valuation that already assumes leadership across rockets, satellite internet and future AI infrastructure. For the stock to deliver extraordinary gains from this level, SpaceX does need to succeed. It needs to exceed expectations that are already extremely high.

Do IPOs usually perform as well as investors expect?

The market remembers the IPO winners. It often forgets the long list of listings that delivered ordinary or disappointing returns.

Across more than 9,000 operating-company IPOs from 1975 to 2021, around 60% finished flat or lower three years after the first close. Only 16% more than doubled. The average return was positive, but that average was lifted by a small group of major winners.

IPO excitement can be powerful, especially when the company is famous. But buying a famous IPO is not the same as buying early. In many cases, the public market receives the asset only after private investors have already captured the steepest part of the return curve.

SpaceX may still become one of the winners. But history is clear: IPO size and investor excitement do not guarantee strong long-term returns.

Source: Yahoo Finance

Could SpaceX’s record IPO drain liquidity from other growth trades?

A $75 billion IPO is not a normal listing. A deal that large can absorb liquidity from other high-growth parts of the market. The same investors who want SpaceX may already own AI stocks, speculative technology names, crypto-linked assets or other expensive growth trades. To make room, some funds may need to sell something else.

That does not mean SpaceX would damage the whole market. But it could become a test of risk appetite. If investors treat SpaceX as the cleanest way to own rockets, Starlink and AI infrastructure in one stock, other high-multiple growth names may lose some attention and capital. The IPO would not only be a company event. It could become a market event.

Can SpaceX be a great company but a difficult stock?

SpaceX is coming to market because it has already become one of the most important private companies in the world. The issue is whether public investors are getting enough upside after that success has already been reflected in the valuation.

Starlink still needs to keep expanding. Launch demand must remain strong. Starship needs to justify heavy investment. AI infrastructure ambitions need to become more than a powerful narrative. And the company must turn scale into durable earnings, not only revenue growth.

At $1.75 trillion, SpaceX does not need a good story. It needs a story that keeps getting better. For now, demand shows investors want access. The harder test comes after the listing, when the market stops rewarding scarcity and starts judging execution.

SpaceX may be a historic IPO. But historic IPOs do not always become historic investments. That is why the real question is not whether SpaceX is important.

It is whether investors are being paid enough to buy it this late.