Global equities weaken amid oil rally and inflation risks; US labour market steady

Global equity markets retreated as surging oil prices, driven by escalating conflict in the Middle East, intensified concerns regarding inflationary persistence. Despite robust corporate earnings for the first quarter of 2026 and a resilient US labour market, major US indices closed lower.

Brent crude reached $105 per barrel as hostilities in the Middle East persisted; Iran’s rejection of ceasefire proposals pending the reopening of US-blocked ports has sustained global inflationary fears.

US jobless claims indicated continued labour stability, leading to a 75% market probability that the Federal Reserve will maintain current interest rates for ahead meetings.

Major US indices declined despite 82% of S&P 500 firms exceeding Q1 estimates, as geopolitical instability and energy overheads overshadowed strong corporate performance.

Tesla shares fell by 3.5% notwithstanding an earnings beat, pressured by a 10% quarter-on-quarter (QoQ) revenue decline and stagnating growth across Chinese and international markets.

Oil prices rise as geopolitical instability persists: Stock markets retreat amid inflationary risks

The primary oil benchmarks rose in tandem as geopolitical instability in the Middle East showed no signs of abatement. The Brent futures contract (BRNM6) reached the $105 level, representing a daily increase of 3.10%. Concurrently, the West Texas Intermediate (WTI) futures contract (CLM6) traded at approximately $96.50 per barrel, up 3.86%. Market participants remain focused on the potential duration of the US–Israel–Iran conflict and the subsequent long-term implications for the global economy.

Earlier this week, US President Donald Trump announced an indefinite extension of a ceasefire offer, pending an Iranian proposal to reach a bilateral agreement. However, Iranian officials have stated that the country will not consider a cessation of hostilities until the US Navy lifts its blockade on Iranian ports. Consequently, military tensions in the region continue to escalate.

This geopolitical volatility has significantly impacted energy prices, creating mounting concerns regarding economic pressures—most notably, the risk of resurgent inflation and a potential global economic deceleration should central banks adopt a more restrictive monetary stance to stabilise prices. This macro environment weighed on US equity valuations at the market close. According to LSEG data, approximately 82% of the 123 S&P 500 companies that have reported Q1 2026 financial results surpassed analyst estimates. Despite these solid fundamentals, the S&P 500 dropped by 0.41%, the Dow Jones Industrial Average decreased by 0.36%, and the Nasdaq 100 depreciated by 0.57%.

In Europe, similar downward pressure was observed: the UK FTSE 100 decreased by 0.19%, the Spanish IBEX 35 fell by 0.67%, and the German DAX 40 depreciated by 0.16%.

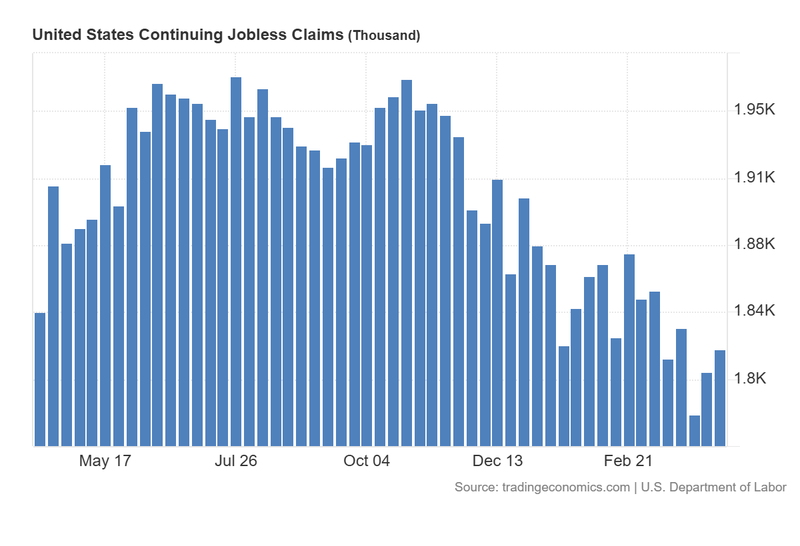

US continuing jobless claims exceed forecasts but signal stable performance

According to data from the US Department of Labour, continuing jobless claims increased from 1,809,000 to 1,821,000 in the latest weekly assessment, slightly exceeding the analyst estimate of 1,820,000. Similarly, initial jobless claims rose by 214,000, marginally above the forecast of 212,000. Although both indicators surpassed estimates, they continue to signal overall labour market stability.

As illustrated in the figure 1, there has been a notable downward trend in continuing jobless claims since October 2025, suggesting that unemployment remains well-contained. Furthermore, the most recent unemployment rate release showed a slight decrease at the 4.3% level, reinforcing the narrative of a stabilising job market.

Consequently, market probabilities suggest that the Federal Reserve is unlikely to implement interest rate cuts in the immediate future, given that the labour sector remains resilient while inflationary pressures persist. According to the CME FedWatch Tool, there is a probability of over 75% that the Federal Reserve will leave rates unchanged for forthcoming sessions, extending through the April 2027 meeting based on current futures pricing.

Figure 1. US Continuing Jobless Claims (2025-2026). Source: Data from the US Department of Labour; Figure obtained from Trading Economics.

Tesla shares retreat despite higher-than-expected Q1 2026 report

Tesla’s shares declined by 3.56% to $373.72, despite reporting solid earnings for the first quarter of 2026. The company’s total revenue and earnings per share (EPS) exceeded analyst forecasts, with the electric vehicle manufacturer recording total revenue of $22.39 billion against an anticipated $22.10 billion. Furthermore, the company achieved an EPS of $0.41, outperforming the market consensus of $0.35. These figures represent a year-on-year (YoY) growth rate of 15.7% in revenue and a substantial 52% increase in EPS.

However, while the Q1 2026 results demonstrate underlying fundamental strength, the company has yet to eclipse the peaks reached in Q3 2025, when total revenue reached $28.09 billion and EPS stood at $0.50. For the current period, Tesla experienced a 10% quarter-on-quarter (QoQ) decrease in revenue and an 18% QoQ decline in EPS.

Additionally, Tesla’s financial statements indicate a deterioration in performance across international segments. Sales in China remained stagnant throughout 2025, while revenue from other international markets (excluding the US and China) decreased by 9.5% over the full 2025 fiscal year.