Strait of Hormuz tensions bolster oil prices; US existing home sales retreat

Escalating tensions in the Strait of Hormuz have propelled oil prices toward the $100 threshold as the United States threatens a maritime blockade. Concurrently, US existing home sales have retreated to a 2025 low, with mortgage rates climbing to 6.37%, reflecting a broader environment of economic uncertainty and heightened consumer caution.

US blockade threats in the Strait of Hormuz have spiked Brent crude to $99.36, jeopardising 20% of the global oil supply and threatening European fuel security.

Bullion retreated to $4,767 as expectations of a restrictive Federal Reserve policy bolstered the US dollar, becoming gold more expensive for foreign investors.

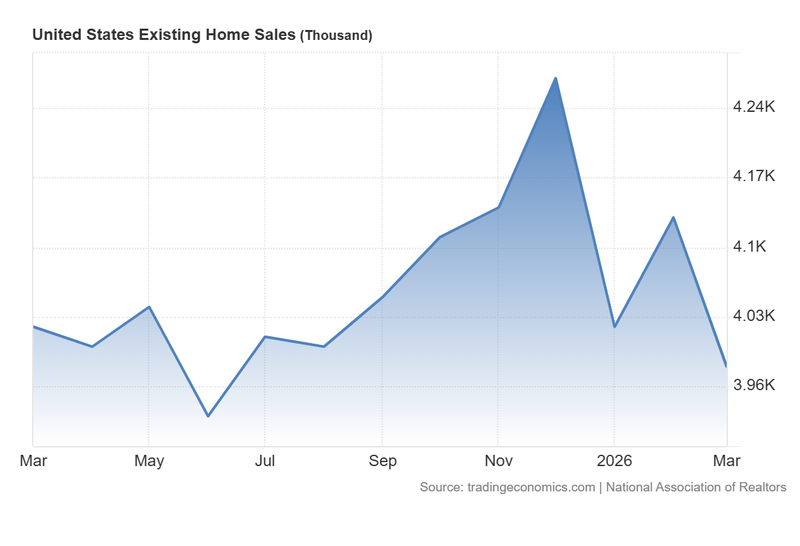

US existing home sales fell to 3.98 million in March—the lowest level since mid-2025—as 30-year mortgage rates have reached the 6.37% zone.

Investors are bracing for further volatility with Q1 2026 earnings from J.P. Morgan and Goldman Sachs, alongside pivotal GDP releases from China and the United Kingdom.

Strait of Hormuz tensions propel oil prices, while gold retreats

According to reports from the White House, the United States is considering a blockade of the Strait of Hormuz, significantly escalating tensions between Washington and Tehran. The Strait remains a critical maritime chokepoint, facilitating the transit of approximately 20% of the global supply of petroleum and natural gas, as well as essential fertilisers and other commodities.

Following the collapse of US–Iran negotiations held last Saturday in Pakistan, President Donald Trump announced a potential maritime intervention—threatening the destruction of Iranian vessels—generating acute concerns over a protracted disruption to global supply chains. In response, Iranian officials have asserted that no regional port will remain secure if their own maritime infrastructure is threatened.

As global energy and food security hang in the balance, European nations appear particularly vulnerable. Reuters reports that approximately 62% of Europe's fuel imports and 42% of its diesel originate from the Middle East, highlighting the continent's exposure to regional instability.

Market reactions were swift, with energy commodities advancing in tandem. The Brent futures contract (BRNM6) rose 4.37% to $99.36, while the West Texas Intermediate (WTI) futures contract (CLK6) increased by 2.79% to $99.13 per barrel. Similarly, gasoline futures (RBK6) appreciated by 2.46% to reach $3.11 per gallon.

In contrast, gold prices edged lower during a highly volatile session. At the market close, bullion fell 0.45% to $4,767 per ounce. The precious metal is currently facing conflicting momentum: while a strengthening US dollar and rising expectations of a hawkish Federal Reserve could render sovereign bonds more attractive—thereby reducing demand for non-yielding assets—the metal continues to see support from hedgers seeking refuge amidst heightened geopolitical and economic instability.

US existing home sales fall short of analyst expectations

Data from the National Association of Realtors (NAR) reveals that US existing home sales declined from 4.13 million in February to 3.98 million in March, missing the analyst consensus of 4.06 million. This reading represents the lowest volume since June 2025, indicating that underlying demand is contracting as geopolitical and economic uncertainty weighs on the consumption of long-term assets. On a month-on-month basis, sales fell by 3.6% in March.

This downturn is likely attributed to two primary factors: a decline in buyer confidence and the steady ascent of long-term interest rates driven by persistent inflationary risks. According to Freddie Mac, the 30-year fixed mortgage rate—the primary benchmark for the US residential market—has reached 6.37%. Compared to February’s level of 5.98%, the benchmark has surged by 39 basis points.

Figure 1. US Existing Home Sales (2025-2026). Source: Data from the National Association of Realtors; Figure obtained from Trading Economics.

Quarterly US financial results

The first-quarter 2026 earnings season begin this week. The following major institutions are scheduled to report, which is expected to contribute to further volatility across US equity markets:

- Monday: Goldman Sachs (GS)

- Tuesday: JPMorgan Chase (JPM), Johnson & Johnson (JNJ), Wells Fargo & Co (WFC), Citigroup (C), BlackRock (BLK)

- Wednesday: Bank of America (BAC), Morgan Stanley (MS)

- Thursday: Netflix (NFLX), PepsiCo (PEP), Abbott Labs (ABT), The Charles Schwab Corp (SCHW)

Key economic events this week

During this week, several key economic indicators will be released. Some of the most important are the following:

Monday

- US: Existing Home Sales

Tuesday

- Australia: Westpac Consumer Confidence

- China: Balance of Trade

- US: Producer Price Index

Wednesday

- US: EIA Crude Oil Stocks Change

Thursday

- China: GDP Growth Rate

- United Kingdom: GDP Growth Rate