Dollar weakens as hopes for Middle East de-escalation

The US dollar weakened sharply as markets reacted to growing signs that the Middle East conflict may be moving closer to a diplomatic resolution rather than further escalation.

Iranian officials described the proposal as an “American Wishlist.”

Investors rotated back into equities and other risk-sensitive assets.

The dollar is no longer moving only on economic data or Fed speeches.

American wish list

The shift in sentiment came after Trump said the US would end its military campaign and lift the Hormuz blockade if Iran agrees to the framework already discussed, though he added that this may be “a big assumption.” He also warned that military strikes would resume if Tehran rejected the proposal.

Iran is currently reviewing the offer and is expected to respond through Pakistan within the next 48 hours. While some Iranian officials reportedly described the proposal as an “American Wishlist,” others acknowledged that significant progress has been made in negotiations.

Possibility of de-escalation triggered a reversal in Dollar positioning

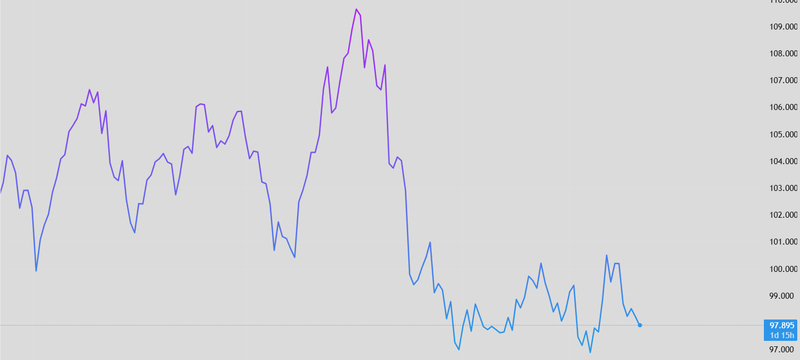

During the conflict, the dollar benefited heavily from risk aversion as it rose 5%, rising oil prices and expectations that the Federal Reserve would need to maintain a more hawkish stance if energy-driven inflation stayed elevated. As a result, the DXY strengthened as investors moved capital toward US assets and defensive positioning.

Source: Trading View

Part of that trade is beginning to unwind

As geopolitical fears eased, investors rotated back into equities and other risk-sensitive assets, reducing demand for the dollar’s traditional safe-haven role. Oil prices also pulled back from recent highs, which further weakened support for the DXY by lowering expectations for prolonged inflation pressure and higher-for-longer US interest rates.

That relationship matters because energy prices became one of the main reasons markets recently shifted back toward a more hawkish Fed outlook. Higher oil prices raised concerns that inflation could remain sticky for longer, forcing policymakers to delay rate cuts or even consider additional tightening if second-round effects appeared.

Dollar’s outlook is still far from straightforward

The dollar may have lost some of its safe-haven strength as tensions eased, but the bigger question is what happens next and that depends largely on oil.

The market is now trying to figure out how quickly crude can move back toward pre-war levels, and whether the inflation shock from the recent spike has already left a deeper mark on the economy. That is the difficult part. Oil can come down fast, but the effects of higher energy costs usually do not disappear at the same speed.

Shipping costs do not overnight. Transport expenses stay elevated for a while. Businesses that absorb higher fuel costs often pass through more slowly. That means inflation can stay sticky even after oil itself starts cooling.

That matters for the Fed

Even if geopolitical tensions improve, policymakers may not feel comfortable changing tone too quickly if inflation data still reflects those energy pressures. The Fed has already learned how costly it can be to underestimate inflation persistence.

If markets become more confident that the conflict is winding down and oil keeps easing, the dollar could stay under pressure. That would likely bring back stronger expectations for rate cuts and push investors further into equities, emerging markets, and higher-yielding currencies.

On the hand U.S. Money supply has climbed to a record $22.7 trillion, the Federal Reserve is still holding borrowing costs high, which should normally slow things down. But money in the system is still growing. That suggests the economy is absorbing higher rates better than expected, and liquidity is staying stronger than many thought.

The opposite risk is still very real

If oil holds up or inflation refuses to cool as expected, the market will have to rethink how quickly the Fed can ease. And once rate-cut expectations get pushed back, the dollar tends to find support again.

The dollar is no longer moving only on economic data or Fed speeches. Right now, it is reacting to a much wider mix geopolitics, energy markets, and how those two reshape the timing of U.S. monetary policy. And until that picture becomes clearer, volatility in the dollar is unlikely to fade.