ECB caught between inflation credibility and weak growth

The euro area is moving back into the kind of policy problem central banks really do not like. Inflation is rising again, not because demand is booming, but because energy prices and geopolitical risk are pushing costs higher. At the same time, growth is already losing momentum.

If the economy contracts by around 0.2%, the ECB will face inflation above the target along with negative growth.

The ECB has spent the past few years working to show it can control inflation after the 2022 energy shock.

This shock may not be as severe as 2022, but the dilemma is familiar.

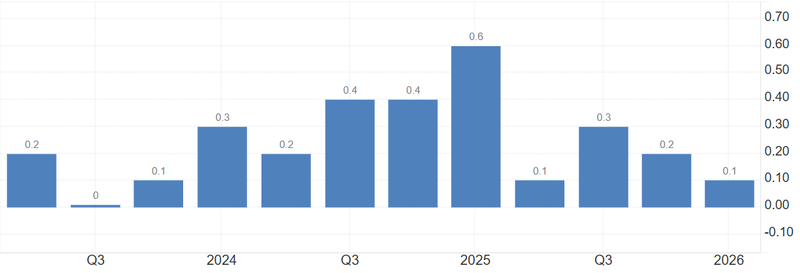

Growth is already too weak for comfort

The eurozone barely grew in the first quarter. This is important because it means the economy entered this energy shock with little protection. Higher fuel and power costs hit Europe quickly. They strain households with utility bills, pressure companies with higher input costs, and weaken confidence when consumers already feel cautious. As a result, businesses delay investment, households cut back on spending, and the slowdown worsens. That is why the second quarter is crucial. If the economy contracts by around 0.2%, the ECB will face inflation above the target along with negative growth.

Source: EUROSTAT

Rehn is trying to defend the ECB’s credibility

The ECB has spent the past few years working to show it can control inflation after the 2022 energy shock. This history matters. If inflation rises again and the central bank seems too passive, markets may begin to doubt its willingness to act when a decision gets politically tough. That is why Rehn’s message sounds more aggressive than the growth data alone would suggest.

He is not just responding to April’s inflation number. He is warning that if the ECB waits too long, controlling inflation expectations could become harder. Once that happens, the central bank would need to take tougher measures later, possibly in an even weaker economy.

The problem is that higher rates would hurt

Higher borrowing costs would add pressure on households, companies and governments. It would tighten financial conditions at the same time energy prices are already eating into real income. The most exposed parts of Europe, especially energy-intensive industries and more debt-sensitive economies, would feel that pressure first.

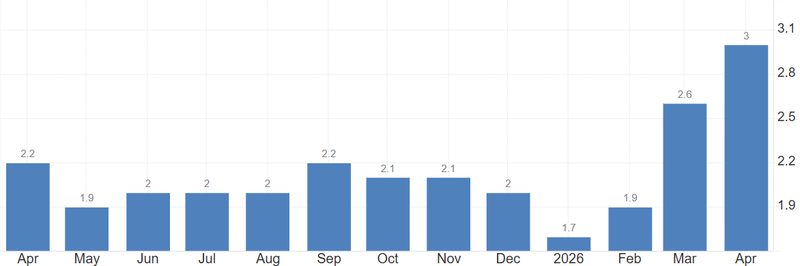

This is why the ECB cannot treat 3% inflation like a normal overheating problem. Higher interest rates cannot produce more oil or gas. They cannot fix a geopolitical supply shock. What they can do is reduce demand and protect inflation expectations.

Source: EUROSTAT

Markets are now facing a less friendly ECB story

For investors, the message is becoming less comfortable. Earlier in the year, weaker growth would have been seen as a reason for the ECB to stay patient or even prepare for easier policy. Now the story is more complicated. If energy prices keep inflation elevated, the ECB may need to stay hawkish even as growth weakens. That is a difficult mix for European assets.

The Euro could get some support from higher rate expectations, but only up to a point. If those expectations are driven by stagflation rather than stronger growth, the currency story becomes much less clean. Equities face the same problem: weaker demand, higher discount rates and margin pressure from rising costs.

The ECB wants time, but the data may not give it much

Rehn is still trying to keep the message balanced. The ECB is not committing to a fixed path, and policy will depend on the next round of data, updated forecasts, energy prices and the geopolitical backdrop.

If April’s inflation rise becomes a trend, and if second-quarter growth confirms a contraction, the ECB’s June decision becomes much harder. It would have to decide whether the bigger risk is tightening too much into a weak economy or waiting too long and damaging its inflation credibility.

Europe is back in an uncomfortable place

Europe has been here before. Energy shocks lift inflation, households lose purchasing power, industry slows, and the central bank is left trying to defend price stability without making the downturn worse.

This shock may not be as severe as 2022, but the dilemma is familiar. Growth is weak, inflation is moving the wrong way, and geopolitical risk is making the outlook harder to predict. That is why Rehn’s warning matters. The ECB is not just watching another inflation print. It is watching whether the euro area is slipping into a phase where inflation stays too high even as the economy loses speed, the central bank still has some room to judge the data. But if inflation keeps climbing and growth slips into contraction, that room will shrink quickly.