Japan inflation pressure puts Takaichi and the BOJ on opposite sides

Japan is moving into a more uncomfortable policy phase. Prime Minister Sanae Takaichi is preparing extra fiscal support to soften the hit from rising fuel and electricity costs, while producer inflation is accelerating fast enough to put new pressure on the Bank of Japan to raise interest rates. The problem is that both sides are responding to the same shock in very different ways.

Prime Minister Sanae Takaichi is considering a supplementary budget to ease rising fuel and utility costs.

Japan’s PPI rose 4.9% year-on-year in April, the fastest pace since May 2023.

Stronger price pressure is increasing speculation that the Bank of Japan may need to raise rates as early as June.

Japan’s inflation problem is becoming harder to manage

Japan’s government is trying to protect households from another squeeze in living costs, but the timing is difficult. Takaichi is considering a supplementary budget aimed at reducing the burden from higher gasoline, electricity and gas prices, with fresh measures potentially focused on the summer months when energy demand rises.

Higher fuel and utility bills hit consumers quickly, especially in an economy where wage growth has often struggled to keep up with inflation. But the market is not looking at this only as household support. It is also asking whether more fiscal spending will make the Bank of Japan’s job harder.

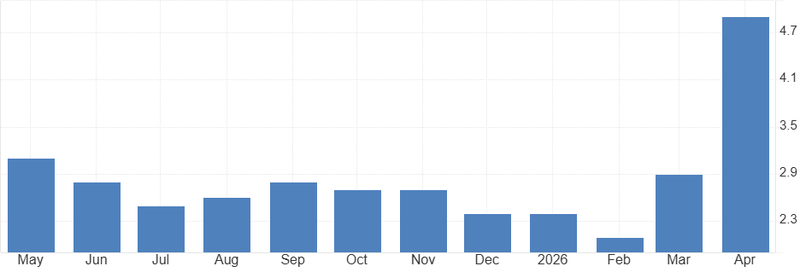

Producer inflation is moving faster than expected

The latest producer-price data has made the inflation story harder to dismiss. Japan’s producer prices rose 4.9% from a year earlier in April, up from 2.9% in March and well above expectations of around 3%. It was the fastest annual increase in nearly three years.

That matters because producer inflation often shows pressure building before it reaches consumers. Companies facing higher input costs can absorb them for a while, but not forever. If energy, chemicals and imported goods remain expensive, the risk is that more of those costs eventually move through the supply chain.

Source: BoJ

Takaichi wants relief, but the BOJ may see risk

The government’s instinct is to cushion the shock. That means subsidies, support measures and possibly a larger budget package. But for the BOJ, that same support can look uncomfortable if it keeps demand firmer while inflation is already moving higher.

This is the policy contradiction Japan now faces. Fiscal policy is trying to soften the pain, while monetary policy may need to lean against inflation. Both responses can be justified, but together they send a messy signal to markets.

If the government spends more to offset energy prices, households get relief. But if investors believe that spending adds to borrowing needs or delays the inflation adjustment, long-term yields could rise further. That is why the budget discussion matters beyond politics.

The BOJ is under more pressure to act

The stronger producer-price data has increased pressure on the Bank of Japan to consider another rate hike. Some officials are now seen as more open to action as early as June, especially if price pressure continues to spread beyond energy.

The BOJ does not want to move too aggressively and damage the recovery. But it also cannot ignore inflation that keeps surprising to the upside. The longer it waits, the greater the risk that markets begin to question whether policy is still behind the curve.

That is the real issue for the yen and Japanese bonds. The question is no longer whether Japan has inflation. It clearly does. The question is whether the BOJ is prepared to respond before inflation expectations become harder to control.

Japan is entering a more difficult policy trade-off

For now, Japan is trying to do two things at once: protect households from higher energy bills and convince markets that inflation will not get out of control. That is not impossible, but it is becoming harder.

Takaichi’s supplementary budget may help soften the immediate cost-of-living squeeze. But the stronger producer-price data means the BOJ has less room to stay patient.

And that is what makes this moment important. Japan’s inflation problem is no longer just about prices rising. It is about whether fiscal policy and monetary policy can move in the same direction or whether markets start to see them pulling against each other.