Inflation leaves Warsh facing a harder Fed test before he even begins

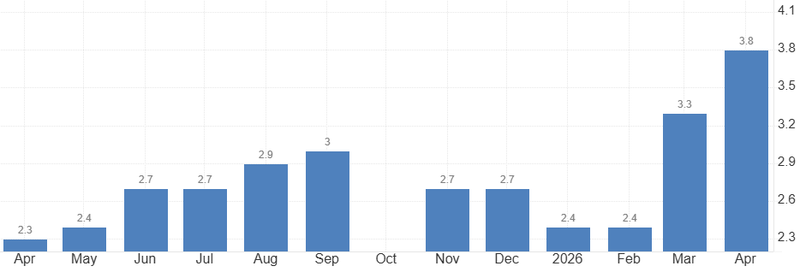

US inflation rose to 3.8% year over year, immediately pushing Treasury yields higher, markets have almost fully priced out Federal Reserve rate cuts for 2026. Odds of a quarter-point rate hike by December have climbed to around 28%.

A stronger dollar here reflects a more uncomfortable macro environment.

Expectations for a quarter-point rate hike by December have climbed to around 28%.

The June meeting is now shaping up as an early test of Warsh’s independence.

The dollar is benefiting from a more hawkish policy path

Treasury yields moved higher, rate-cut expectations faded, and the dollar found renewed support. That is the classic response when investors believe the Fed will stay tighter for longer.

But this is not a clean positive dollar story. A stronger dollar here reflects a more uncomfortable macro environment: higher inflation, higher yields and less room for policy support. It may attract capital, but it also tightens financial conditions at a time when consumers are already under pressure from fuel and living costs.

In other words, the dollar is benefiting because the Fed is trapped, not because the outlook has suddenly improved.

Inflation has shifted the Fed debate again

The latest US inflation report has made the Federal Reserve’s path harder, not easier. Consumer prices rose 3.8% year over year, a hotter reading that immediately pushed Treasury yields higher and reinforced the idea that the Fed may have little room to cut rates this year.

The problem is not only that inflation is above target. It is that the direction is moving against the easing story markets had been trying to price earlier in the year. Energy costs remain the main driver, but the risk for policymakers is that the shock does not stay contained in gasoline and fuel. Once higher transport and input costs begin moving into food, services and consumer expectations, the Fed’s ability to dismiss the inflation spike becomes much weaker.

Source: U.S. Bureau of Labor Statistics

Rate cuts are being pushed out of the conversation

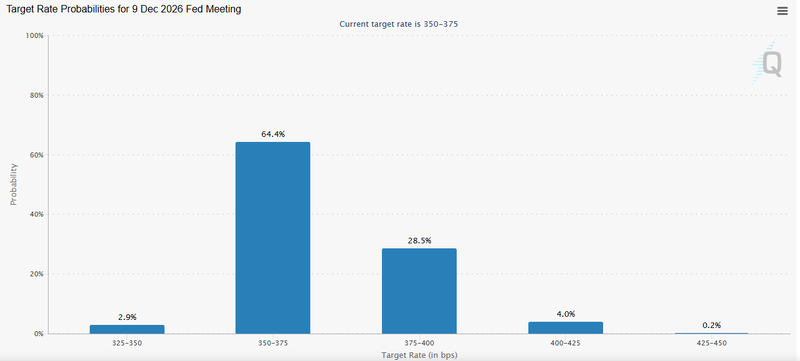

Markets have completely priced out the possibility of Federal Reserve rate cuts in 2026. Instead, the debate is beginning to move in the opposite direction. Expectations for a quarter-point rate hike by December have climbed to around 28%, a sharp shift from the earlier assumption that the next move would eventually be lower.

That shift has also helped to drive capital back into the dollar. When inflation rises and the Fed is forced to stay restrictive, the dollar usually benefits from higher rate expectations and renewed demand for yield. The move is not necessarily about confidence in the US economy. It is more about the market, accepting that US rates may stay higher than previously expected.

Source: CME Group

Warsh inherits a central bank with limited room to move

Kevin Warsh is expected to take over the Fed at a moment when the political demand for lower rates is rising, but the economic case for cutting is weakening. His first interest-rate meeting is expected to come on June 16–17, assuming the confirmation process is completed as expected.

Trump has made clear that he expects lower borrowing costs. That expectation is politically understandable. High mortgage rates, expensive credit and rising fuel costs are all damaging for households and businesses. But the Fed cannot cut rates simply because the administration wants relief, especially with inflation moving further away from the 2% target.

Internal opposition could become the real constraint

Even if Warsh wanted to move aggressively toward rate cuts, he would not control the Fed alone. The Federal Open Market Committee remains full of officials who are likely to stay cautious as long as inflation is sticky and energy-driven price pressures remain unresolved.

That creates an internal constraint. A chair can shape the message, guide the discussion and influence the policy framework, but he still must build consensus. If Warsh pushes too hard for cuts while inflation is rising, he risks facing resistance from voting members who are more focused on credibility than political pressure.

That is where the risk becomes institutional. A divided Fed would make communication harder, weaken market confidence and raise questions about whether policy is being driven by inflation data or by the White House.

Warsh’s first test may be whether he refuses to move too quickly

The June meeting is now shaping up as an early test of Warsh’s independence and credibility. Markets will not only listen to what they say about inflation. They will listen to whether he sounds like a Fed chair responding to the data, or a political nominee trying to satisfy the administration.

If Warsh signals patience, he may disappoint Trump but reassure markets that the Fed is still focused on inflation control. If he opens the door too quickly to cuts, investors may question whether the central bank is prepared to defend price stability at a time when inflation is already moving higher.