Oil deficit widens as Trump turns to China and Russia gains from higher prices

The oil market is tightening again, and the political pressure around it is becoming harder to ignore. The EIA now expects global inventories to fall by an average of 2.6 million barrels a day in 2026.

A drawdown of 2.6 million barrels a day is not a small adjustment.

Trump claim that China has agreed in buying more US crude came at a sensitive moment.

Russia oil export revenue estimated around $19.18 billion.

Oil is moving from shock pricing to deficit pricing

The oil story is no longer only about geopolitical fear. It is becoming a more structural concern about whether the market has enough spare supply and inventory cushion to absorb a prolonged disruption.

That is why the latest inventory forecasts matter. A drawdown of 2.6 million barrels a day is not a small adjustment. It means the global oil market is consuming its safety buffer at a pace that leaves very little room for new shocks. When inventories fall this quickly, prices do not need a fresh escalation to stay supported. They only need the current disruption to last longer than expected.

The IEA’s warning adds to that pressure. The agency has already flagged that global supply losses linked to the Middle East conflict are draining inventories rapidly, while high prices are starting to damage demand. That is the uncomfortable balance now facing the market: demand may weaken, but not quickly enough to fully offset the supply hole.

Source: MacroMicro

Trump is trying to turn energy into diplomacy

President Trump’s claim that China has agreed, or at least shown interest, in buying more US crude came at a sensitive moment. Oil prices were already firm because of tight supply, and the idea of China stepping back into US energy purchases gave the market another reason to price stronger demand for American barrels.

The White House said Chinese President Xi Jinping showed interest in buying more US oil, partly to reduce reliance on the Strait of Hormuz. Chinese state media, however, did not confirm a concrete energy agreement, and Beijing has not publicly committed to large-scale purchases. That leaves the market pricing possibility rather than certainty. Still, in a tight oil market, possibility is enough. If China meaningfully increases US crude purchases, it could help redirect some trade flows and ease pressure on vulnerable routes. If it does not, the statement may still serve Trump politically by showing that he is trying to use trade diplomacy to contain the energy shock, the problem is that oil traders do not wait for full confirmation. They move first, especially when inventories are already falling.

Russia is benefiting from the price shock

The other side of the story is Russia. Despite production losses, sanctions pressure and continued attacks on its energy infrastructure, higher global prices are helping Moscow recover revenue. Reports show Russia’s oil export revenues rose sharply, with April revenue estimated around $19.18 billion, up more than $6 billion from a year earlier.

That matters because it complicates the geopolitical impact of the oil shock. Western sanctions were designed to limit Russia’s ability to profit from energy exports, but the latest price move shows their limits. Discounts, shipping restrictions and price caps may have changed how Russian oil is sold, but they have not fully stopped Moscow from earning substantial revenue when global prices rise.

The same high prices hurting consumers in the US, Europe and Asia are also giving Russia more financial room. Even if production volumes are lower, the price effect can still dominate. In other words, sanctions may reduce efficiency and narrow Russia’s options, but they do not erase the basic advantage of being an oil exporter in a tightening market, supply disruption is not only inflationary it can also redistribute financial power toward producers that remain able to export into a tight market.

Markets are watching inventories more than promises

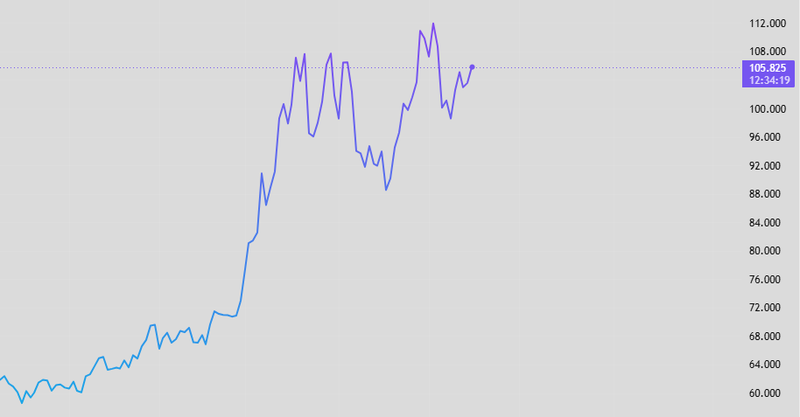

Oil prices are reacting to every diplomatic headline, but the deeper driver is now physical tightness. Brent has been trading above $100 a barrel, while WTI has also remained elevated as traders weigh limited flows, stronger refining margins and the risk that summer demand worsens the drawdown.

That does not mean prices can only move higher. Demand destruction is real. Consumers eventually adjust to higher fuel prices, airlines begin cutting flights, refiners reduce processing activity, and governments may tap strategic petroleum reserves to ease pressure. But those mechanisms move slowly, and none of them can immediately replace barrels that disappear from the market during a supply shock.

Source: Trading View

A tighter market gives oil a stronger political role

Trump needs lower fuel prices before the economic pain becomes more visible at home. China may use energy purchases as part of a wider negotiation with Washington. Russia is gaining revenue from a price shock it did not fully create but is clearly benefiting from.

That is why the deficit warning matters. It changes the tone of the market. This is no longer just a short-term surge driven by fears surrounding the Strait of Hormuz. Markets are now starting to question whether global supply chains, strategic petroleum reserves and diplomatic efforts are strong enough to prevent a temporary shock from evolving into a more persistent inflation problem.

For now, the answer is not clear. Prices are supported because the market sees a deficit. Diplomacy is active because governments see political cost. And Russia is benefiting because, in a tight oil market, fewer barrels can still mean more money.