US inflation continues to accelerate as energy keeps pressure on the fed

US inflation is expected to rise to 3.7% in April from 3.3% in March as energy prices remain the main driver, keeping pressure on household costs and inflation expectations and Kevin Warsh’s confirmation process comes at a sensitive moment for Fed credibility.

Inflation is expected to rise to 3.7%.

NFP recorded 115,000 in April.

Warsh is not entering a calm policy environment.

Inflation is moving in the wrong direction again

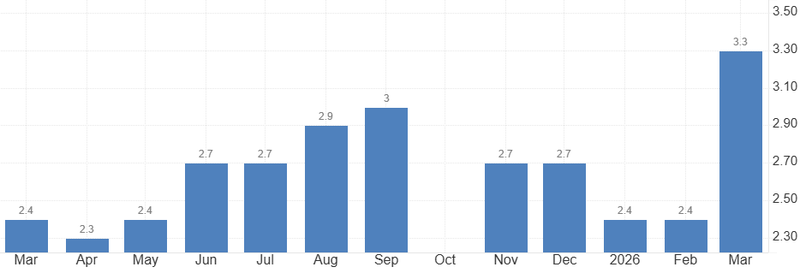

The next US inflation report is arriving at a difficult moment for markets, the Federal Reserve and the White House. CPI is expected to rise to 3.7% in April from 3.3% in March, a move that would reinforce the view that the energy shock from the Middle East conflict is no longer just a temporary market disruption. It is now starting to appear directly in the inflation data.

That matters because the Fed was already dealing with a slow and uneven disinflation process. March CPI showed prices rising 3.3% from a year earlier, with energy up 12.5% and gasoline up 18.9%, If April confirms another acceleration, the debate around rate cuts becomes much harder to defend.

This is not the kind of inflation backdrop that gives policymakers room to move early. It is the opposite. It forces them to wait, watch and avoid sounding too confident about relief that has not yet arrived.

Source: U.S. Bureau of Labor Statistics

Energy is doing damage the Fed cannot easily control

The problem for the Fed is that this inflation pressure is not coming from a clean demand boom. It is being driven heavily by energy, fuel and transportation costs, which are harder for monetary policy to offset without causing damage elsewhere.

Higher fuel prices do not only hit consumers at the pump. They move through freight, food distribution, airline costs and business margins. That is why the April CPI report matters beyond the headline number. If energy costs continue to filter into broader categories, the Fed may have to treat the shock as more persistent than markets initially expected.

This is where the policy risk becomes uncomfortable. A central bank can look through a short-lived oil spike. It cannot easily look through a shock that begins to change inflation expectations.

Rate cuts are being pushed further away

The market discussion has already shifted. Earlier in the year, investors were still debating when the Fed could begin easing. Now the question is whether the Fed can cut at all before late 2026.

Some projections now point to only one 25 basis point cut later in the year, and even that depends on inflation showing signs of stabilizing after the energy shock. If CPI rises to 3.7%, the Fed will have very little incentive to guide markets toward easier policy.

That does not mean the Fed is preparing to hike immediately. The labour market still solid and NFP recorded 115,000 in April, significantly above expectations for a 62,000 increase, and a prolonged energy shock can weaken consumption over time. But it does mean the bar for cuts has moved higher. The Fed can tolerate slower growth more easily than it can tolerate a fresh rise in inflation credibility risk.

Warsh enters the confirmation process at a tense moment

Kevin Warsh’s confirmation process is now unfolding against that backdrop. The Senate is set to move on to cloture for his nomination, with the full confirmation vote expected during the week. His nomination had already cleared the Senate Banking Committee in a 13 to 11 party-line vote, setting up the next stage of the process.

Timing is important. Warsh is not entering a calm policy environment. He is entering one where the Fed’s next chair may immediately face a credibility test: how to respond to inflation that is rising again while political pressure for lower rates remains intense.

Markets want lower rates, but inflation is limiting the story

The political message around Warsh has leaned toward the idea that his leadership could eventually bring lower interest rates and more stability. But markets will not price that story in isolation. They will price it against the inflation data.

If CPI comes in hot, investors may view any push toward easier policy with more caution. A Fed chair can shape tone, communication and committee dynamics, but cannot easily ignore a renewed inflation acceleration without risking credibility.

That is why the CPI release and Warsh vote are connected. One is economics. The other is institutional. Together, they define the Fed’s near-term problem.