Alphabet’s earnings signal the AI infrastructure boom has arrived

Alphabet’s latest earnings were not just strong. They were the kind of numbers that force the market to rethink the scale and speed of the AI cycle inside Big Tech.

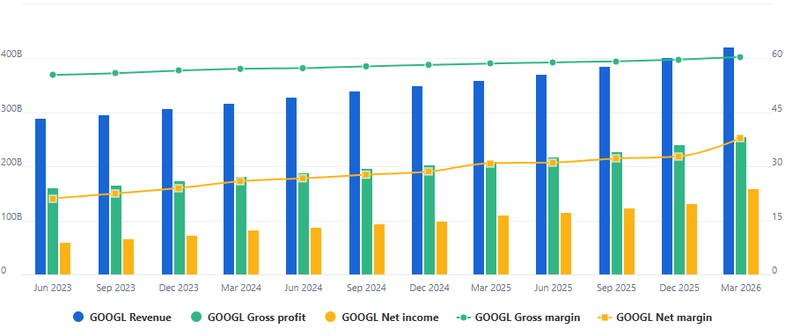

Revenue came in at $109.9 billion, up 22% from a year earlier.

Google Cloud crossed $20 billion in quarterly revenue for the first time.

Price could begin targeting the psychological 450 level.

Alphabet strong earnings

Alphabet’s latest earnings were not just strong. They were the kind of numbers that force the market to rethink the scale and speed of the AI cycle inside Big Tech.

Revenue came in at $109.9 billion, up 22% from a year earlier, while earnings per share reached $5.11 almost double analyst expectations of $2.62. That is not the profile of a company merely benefiting from AI enthusiasm. It is the profile of a company already monetizing it aggressively.

Source: Fullratio

Important detail may not even have been the headline beat itself.

Google Cloud crossed $20 billion in quarterly revenue for the first time, a milestone that says far more about where Alphabet’s business mix is heading than any single earnings figure. For years, investors viewed Google Cloud as the expensive challenger trying to catch up with AWS and Microsoft Azure. Now it is increasingly becoming one of Alphabet’s main growth engines. That shift matters because cloud revenue is no longer just infrastructure revenue. In the current environment, cloud growth is effectively becoming AI growth.

The reason is straightforward. Most enterprise AI workloads eventually need massive computing infrastructure, specialized chips and integrated software ecosystems. The hyperscalers are no longer just renting storage and servers. They are becoming the backbone of the AI economy itself.

Alphabet’s TPU announcement reinforced that point directly

The company introduced its eighth-generation TPU chips, designed specifically for “agentic” AI tasks. That language is important because the industry is rapidly moving beyond simple chatbot models toward systems capable of autonomous multi-step reasoning, execution and workflow management, the market is shifting from AI that answers questions to AI that performs tasks.

That transition could become one of the biggest infrastructure buildouts the tech sector has seen in years. Agentic AI requires significantly more compute intensity, faster inference and more specialized hardware optimization than earlier generations of consumer-facing AI tools.

It is showing up in current revenues now.

That does not mean the AI trade suddenly becomes risk-free. Capital expenditure across the industry remains enormous, competition is intensifying, and regulatory scrutiny will likely increase as AI systems become more deeply integrated into business operations.

But the earnings report does strengthen one critical argument bulls have been making for months: the companies building the infrastructure layer of AI may capture the economics sooner than many expected.

The deeper point is that Alphabet no longer looks like a company defending its legacy business against AI disruption. It increasingly looks like one of the companies helping define the next computing cycle itself.

Markets are increasingly pricing Alphabet around AI monetization, cloud expansion, enterprise adoption and operating leverage improvement. Investors appear more confident that products tied to Gemini, Search AI integration, Google Cloud and TPU infrastructure can support stronger revenue growth over the coming quarters.

Technical outlook

GOOGL continues to show one of the strongest long-term uptrends among mega-cap technology stocks, as the market increasingly views Alphabet as an AI and cloud infrastructure leader rather than just an advertising company.

The bullish cycle that started forming in late 2022 became much stronger throughout 2024 and 2025 as institutional buying accelerated. Price has consistently respected the rising trendline, which suggests investors still see Alphabet as a long-term AI winner instead of a short-term momentum trade.

The breakout above the 350 region was especially important technically because it confirmed continuation of the broader uptrend after the earlier correction. Rather than breaking lower after the pullback toward 270, buyers stepped in aggressively and pushed the stock back toward the 380 area.

So far, the structure still looks like a continuation trend rather than a late-stage top. Every correction has produced higher lows, which is usually a sign that buyers remain in control.

Risk in momentum indicators

Momentum indicators are becoming stretched again, with RSI moving back above 70 after recovering sharply from the previous reset. That shows bullish momentum has strengthened significantly.

In strong secular trends, RSI can stay overbought for long periods, especially when institutional money continues rotating into AI leaders and large-cap growth stocks. But elevated momentum also increases the risk of short-term volatility and profit-taking, particularly as prices move further away from long-term support levels.

The scenarios ahead for Alphabet

The bullish scenario depends on Alphabet holding above the 350 breakout zone and continuing to build momentum from current levels. If macro conditions stay supportive and AI growth keeps accelerating, the market could start targeting the psychological 450 region over the medium term.

The bearish scenario starts if momentum weakens near recent highs and the stock fails to hold its breakout structure. In that case, a deeper pullback toward the 320–350 support range becomes more likely, especially if Treasury yields move higher or AI expectations become too aggressively priced in.

Source: Trading View