Europe’s recovery is being tested again

Europe’s recovery was starting to take hold, but the environment has shifted again. A new external shock is feeding through energy markets and trade, just as growth remains fragile. The result is a more complex outlook, where inflation risks are rising and policy choices are becoming harder.

Labour market has remained relatively resilient, with unemployment at 6.2% in February 2026.

ECB could find itself caught between supporting the economy and maintaining price stability.

Upside risks for inflation and downside risks for growth. That combination is exactly why stagflation risks are back in focus.

A fragile economy with limited room to absorb shocks

Europe’s economy is once again facing a difficult balancing act. Just as the euro area had started to show signs of stabilisation, the conflict in the Middle East has introduced a new external shock through energy markets, trade routes and business confidence.

The European Central Bank has already acknowledged that the situation has made the outlook “significantly more uncertain”, creating upside risks for inflation and downside risks for growth. That combination is exactly why stagflation risks are back in focus.

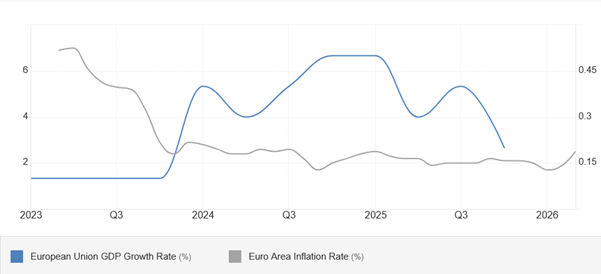

The latest data show that the euro area economy was growing, but only modestly, even before the latest energy shock intensified. GDP rose by 0.2% in the fourth quarter of 2025, with full-year growth for 2025 coming in at 1.4%.

At the same time, the labour market has remained relatively resilient, with unemployment at 6.2% in February 2026, still low by historical standards. On their own, these figures do not point to a recession. However, they do highlight an economy that was already expanding at a fragile pace, with limited capacity to absorb a sudden rise in oil prices and shipping costs.

Inflation returns as the main risk

Inflation is once again the central concern. Euro area headline inflation is estimated to have risen to 2.5% in March 2026, up from 1.9% in February, moving back above the ECB’s 2% target.

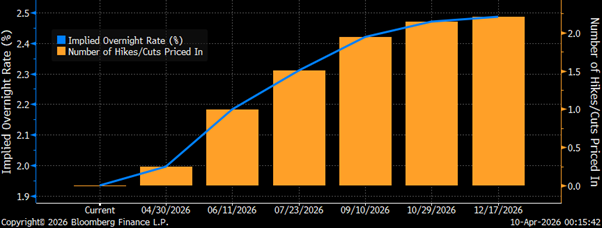

The ECB’s March staff projections had already anticipated inflation averaging 2.6% in 2026, explicitly pointing to higher energy prices linked to the conflict in the Middle East. At the same meeting, the ECB left its key rates unchanged, keeping the deposit facility rate at 2.00%, while stressing that future decisions will remain data-dependent and taken meeting by meeting.

The real risk is that Europe could face the worst of both worlds. Shipping through the Strait of Hormuz has fallen sharply, according to recent reporting, while oil market analysts warn that delayed normalisation could keep Brent prices elevated and push them higher. For Europe, which remains highly sensitive to imported energy costs, this means higher fuel and transport prices feeding into household bills and business input costs just as demand remains soft.

This does not mean a return to 1970s-style stagflation is inevitable. Wage growth, labour market conditions and the duration of the geopolitical shock will all play a role. But the risk is clear: if inflation stays elevated due to energy while growth weakens under uncertainty and tighter financial conditions, the ECB could find itself caught between supporting the economy and maintaining price stability. In that sense, the conflict in the Middle East is no longer just a geopolitical issue for Europe, it is becoming a monetary policy challenge.