Sticky inflation is cornering the BoE

In Q2 the Bank of England is facing a difficult trade-off. Inflation remains stubborn, growth is weak and public finances are under increasing strain. Together, these forces are limiting policy flexibility and reinforcing the case for rates to stay higher for longer.

The most likely scenario is not a strong rebound in inflation, but rather a pause in the disinflation trend.

The BoE is likely to keep interest rates unchanged, allowing time for the effects of previous tightening to filter through.

The combination of persistent inflation pressures and a fragile fiscal position could push the Bank toward a more hawkish stance.

Reacceleration risks emerge

Inflation is no longer moving in one direction. Core inflation has edged up to 3.2%, while services inflation remains elevated at 4.3%. This matters because services are largely driven by domestic wages and demand, making them slower to ease than goods prices.

At the same time, external pressures are starting to build. Renewed tensions in global oil markets have pushed crude prices higher, reflecting both supply risks and geopolitical uncertainty.

For the UK, the impact is less about direct energy bills and more about second-round effects. Rising costs in transport, logistics and production could slow, or even reverse, the recent easing in goods inflation.

Source: Office for National Statistics

The most likely outcome is not a sharp rebound, but a pause in disinflation. CPI is expected to hover between 4% and 5.5%, while core inflation remains above 3%. This keeps inflation firmly above target and reinforces the view that the return to 2% will be gradual, not immediate.

Higher-for-longer returns to the forefront

Higher-for-longer is back in focus. Markets are no longer assuming rate cuts will follow automatically. The Bank’s March survey shows a split view, with expectations ranging from Bank Rate holding at 3.75% to only a modest easing toward 3.50%.

At the same time, growth remains too weak to support a decisive shift. Real GDP was flat in January and up just 0.2% over three months, leaving the Bank of England caught between subdued activity and inflation that is still too high.

Policy is therefore likely to stay on hold as the Bank waits for clearer signs that services inflation is easing. A rate hike cannot be ruled out, but it remains a conditional risk rather than the base case. Markets are pricing in around 52 basis points of tightening by year-end, roughly two hikes, though Governor Andrew Bailey has suggested those expectations may be too aggressive.

For now, the most likely path is patience. Rates are expected to remain restrictive for longer, rather than moving higher in the near term.

Looking ahead, the balance tilts toward stability rather than action. Unless inflation picks up meaningfully, particularly in services, the is likely to hold rates steady and allow previous tightening to continue feeding through. The risk is not an immediate policy shift, but a prolonged period of restrictive conditions.

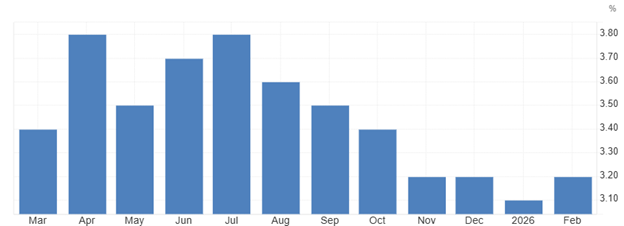

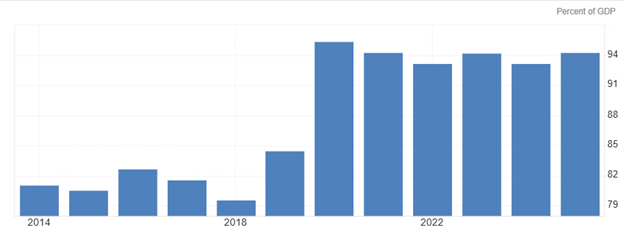

Borrowing adds to fiscal pressure

Public borrowing for the financial year to February 2026 reached £125.9bn, one of the highest levels outside crisis periods, with February alone coming in above OBR forecasts. This is feeding directly into the overall debt burden, pushing the debt-to-GDP ratio back to its 2021 peak at a time when growth is too weak to offset it.

This dynamic keeps fiscal policy closely tied to the interest rate outlook. Higher debt levels make public finances more sensitive to rates staying elevated, as refinancing costs and debt interest payments remain exposed to both yields and inflation. With a significant share of index-linked liabilities, any persistence in CPI feeds directly into government spending, tightening fiscal conditions even without new policy measures.

Looking ahead, this supports the case for policy to remain restrictive. The Bank of England is unlikely to ease quickly while inflation stays above target, particularly given the fiscal backdrop. A rate hike is not the base case, but it cannot be ruled out.

If CPI were to move back towards or above 5%, the combination of persistent inflation and fiscal vulnerability could prompt a more hawkish response, even at the cost of tighter financial conditions.

Source: Office for Budget Responsibility, UK