The Fed is stuck between inflation risk and slowing growth

The Federal Reserve enters Q2 facing a familiar challenge in a more complex form. Markets have reacted quickly, but for policymakers, the real question is what comes next. An energy-driven shock has hit as inflation was easing but not yet under control, while growth is slowing but not breaking. That leaves the Fed with little room for error, making patience the most likely path.

Market volatility may have eased, but the macro impact is only starting to unfold.

Fed faces a supply-driven risk just as inflation was improving but not fully resolved. In that environment, caution becomes the default.

Growth is losing momentum, but employment remains firm enough to justify patience.

Markets have calmed, but the Fed’s problem hasn’t

The two-week ceasefire announced on April 8 helped ease immediate panic across markets. But for the Fed, that does not mean the shock has passed.

The focus has shifted. It is no longer about the initial spike in oil prices, but whether the disruption filters through slower and more persistent channels, freight costs, shipping delays, fuel prices, consumer expectations and broader pricing behaviour.

With transit through the Strait of Hormuz still uncertain and major shipping firms warning that a full return to normal could take weeks, the Fed is left managing a more complex version of a familiar problem. Market volatility may have eased, but the macro impact is only starting to unfold.

Q2 is less about fear and more about timing

This is what makes the second quarter particularly challenging for policymakers.

By the March meeting, the policy debate had already shifted beyond the timing of rate cuts. Minutes show that almost all participants supported keeping rates unchanged, viewing policy as close to a neutral range after 75 basis points of easing in the second half of last year.

More importantly, officials were increasingly concerned about upside inflation risks linked to energy, while still uncertain about how deeply the Middle East shock could affect growth.

That combination leaves little room for decisive action. If growth were collapsing, easing would be clearer. If inflation were falling cleanly, the path would also be simpler. Instead, the Fed faces a supply-driven risk just as inflation was improving but not fully resolved. In that environment, caution becomes the default.

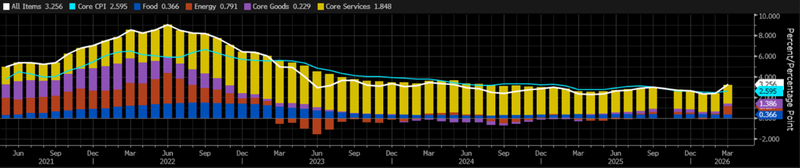

Inflation has picked up, but not across the board

The latest CPI data reinforces why the Fed is likely to remain patient.

Headline inflation rose 0.9% in March, bringing the annual rate to 3.3%. Core inflation was more contained at 0.2% month-on-month and 2.6% year-on-year. The increase was driven largely by energy, with the energy index up 10.9% and gasoline rising 21.2%, while shelter increased 0.3% and food remained unchanged.

For policymakers, this creates an uncomfortable but not decisive signal. Inflation has clearly been impacted by the oil shock, but core dynamics do not yet point to a broad-based reacceleration.

This supports a hold-first approach into the April meeting, as the Fed waits to see whether the energy-driven move remains isolated or begins to spread.

Source: Bloomberg

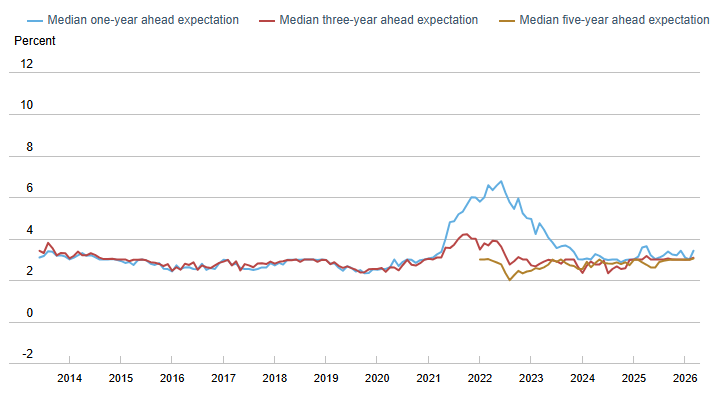

Inflation expectations are becoming more sensitive

The greater risk is not a single spike in inflation, but how households respond to it.

Latest data from the New York Fed shows one-year inflation expectations rising to 3.4% in March, with three-year expectations at 3.1% and five-year expectations holding at 3.0%. Longer-term expectations remain relatively anchored, but the shift suggests households are becoming more sensitive to price risks again.

The sharp rise in expected gasoline inflation reinforces that concern.

Source: newyorkfed

For the Fed, the experience of 2022 still matters. Policymakers are less willing to assume that a supply shock will remain contained. Once expectations begin to adjust, the risk extends beyond energy into wages, services and broader pricing behaviour.

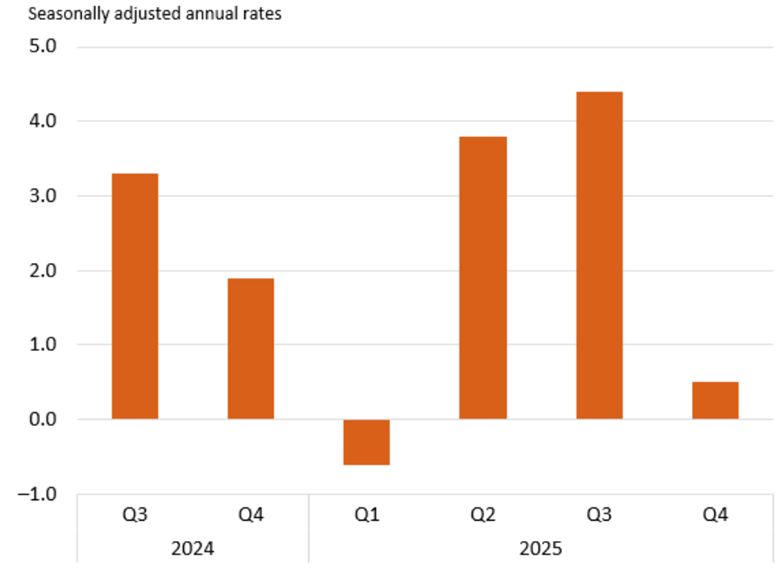

Growth is slowing, but not enough to force action

There is also no clear growth argument for immediate easing.

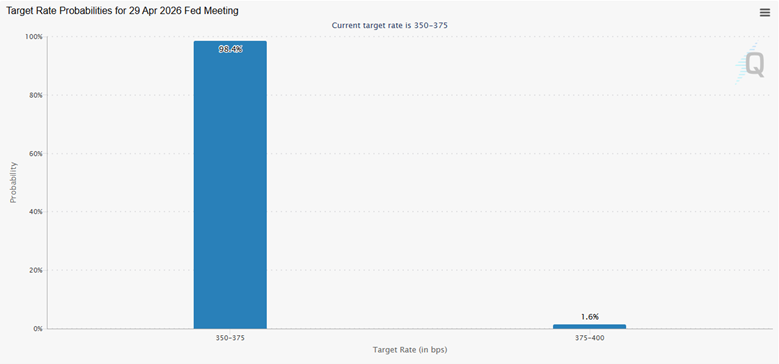

Source: CME Group

Real GDP growth slowed to a 0.5% annualised pace in Q4 2025, down from 4.4% in the previous quarter. That points to a softer economy, but not one weak enough to trigger urgent policy support.

Source: bea.gov

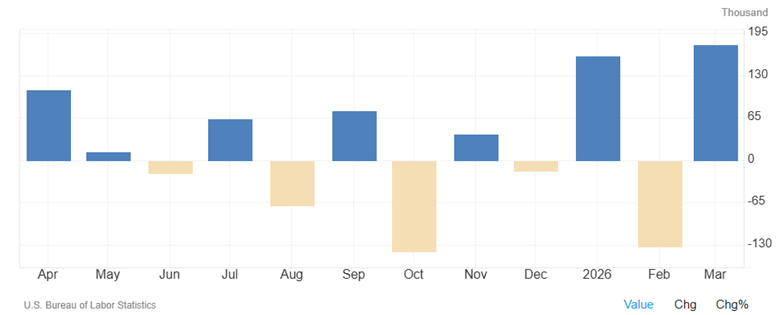

The labour market remains relatively stable. March payrolls increased by 178,000 and the unemployment rate held at 4.3%. While conditions have cooled compared to last year, they have not deteriorated to a level that would force the Fed into a defensive cut.

This leaves policymakers in an uncomfortable position. Growth is losing momentum, but employment remains firm enough to justify patience, especially with inflation risks still present.

Source: US Bureau of Labor Statistics

The Fed is waiting because the outcome is still unclear

The Fed is not waiting because the shock has passed. It is waiting because it does not yet know what the shock becomes.

The ceasefire has reduced the risk of an immediate energy disruption, but it has not restored clarity to the macro outlook. Inflation remains above comfort levels and growth is slowing without collapsing.

The key question is whether this is a temporary energy shock that lifts headline inflation, or the start of a broader pricing dynamic that delays easing further. For now, the most credible path remains steady. Hold rates, monitor how the shock feeds through the economy and avoid reacting before the full impact is clear.